Stolen Trust: A Special Study on America’s Elder Fraud Landscape

← Study overview · Download the study (PDF) · Companion timeline (PDF)

The full text of Stolen Trust: A Special Study on America’s Elder Fraud Landscape, HCSK’s 2026 analysis of elder fraud in the United States, reading federal data and 1,910 news items together. Every figure traces to a federal primary source.

Proudly Featured by

Table of Contents

- Key Findings and the National Ask

- Foreword

- Chapter 1: The Numbers

- Chapter 2: State-by-State Rankings

- Chapter 3: The Four Scams

- Chapter 4: The AI Escalation

- Chapter 5: What 10 Months of News Coverage Reveal

- Chapter 6: Who Is Fighting Back

- Chapter 7: The Legislative Landscape

- Chapter 8: Beyond the Dollar

- Chapter 9: The Proposal: The Three Ones

- Appendices

- Appendix A: About HCSK Inc.

- Appendix B: Glossary of Key Terms

- Appendix C: Methodology

Key Findings

Reported elder fraud reached $7.748 billion in 2025 (FBI IC3, adults 60+), up from $1.685 billion in 2021, a +360 percent five-year increase and eight times the 2020 figure of $966 million. Recovery turns on catching the money within hours, and most reports never reach a federal channel that fast. America has the agencies, the laws, and the data. What this study finds it lacks is a single front door, a single message, and a single clock. Three findings point to the same gap. Chapter 9 sets out a coordinated response we believe could help: the Three Ones.

1

Fragmented intakeTen federal actors handle elder fraud, most through their own hotline, portal, or form. None is dysfunctional. None is the front door.

One Front Door

One national number to call and one website to report, 24/7.

2

Inconsistent messagingAnti-fraud advice is borrowed from cybersecurity and misses the real threat, which is manipulation, not technical exploitation. Seniors get no single rule to fall back on.

One Message

Federal and state agencies adopt one protective rule, Think First, Verify Always.

3

Speed mismatchA fraudulent wire can be frozen only if it is reported within hours, but most reports never reach a federal channel that fast. Once the money clears, recovery is almost impossible.

One Day

A 24-hour coordinated response standard: from agencies to family support.

Chapter 9 proposes a coordinated framework, the Three Ones, built from infrastructure that already exists.

Foreword

Yuksel Aydin

Founder & Director,

HCSK, Human Cybersecurity Knowledge for Seniors

About This Study

In 2025, Americans aged 60 and over reported $7.748 billion stolen to fraud. The FBI’s Recovery Asset Team, the federal government’s main tool for clawing money back, freezes about half the money in the cases caught in time, but almost no case reaches it that fast, so less than half of one percent of the stolen total was frozen. The country is not standing still: ten federal actors, dozens of state units, banks, and platforms fight elder fraud every day. America has the agencies, the laws, and the data.

Stolen Trust: A Special Study on America’s Elder Fraud Landscape is published by HCSK Inc. (https://seniors.hcsk.org), a nonprofit resource focused on online scams targeting older adults, with a special focus on AI-enabled fraud.

Existing federal reports document important parts of the elder fraud crisis. The FBI publishes detailed data on cybercrime complaints. The FTC publishes thorough analysis of consumer fraud demographics. The Consumer Financial Protection Bureau publishes the leading federal framework on what financial recovery actually requires. The U.S. Senate Special Committee on Aging publishes a Fraud Book. Academic researchers produce valuable studies on specific aspects of the problem. Journalists cover individual cases with skill and empathy.

This study’s contribution is to bring those parts together into one picture, the scale, the trajectory, the geography, the criminal mechanics, the human cost, and the structural reasons why so little stolen money is ever recovered (the FBI’s recovery team freezes about half the money in the cases that reach it in time, but almost no case reaches a federal freeze that fast, so under one percent of 2025 losses was frozen) and to respectfully suggest a unifying response framework: the Three Ones.

The Three Ones

After eight chapters of analysis, Chapter 9 proposes a single coordinated framework, built from existing infrastructure, to address three findings about America’s elder-fraud response: no single front door (a dozen actors and reporting sites, with no single number to call or website to visit), inconsistent protective messaging (cybersecurity-borrowed advice that does not address manipulation-based scams), and a speed mismatch between how fast a fraudulent wire must be caught to be frozen and the response timeline.

Its three parts, One Front Door, One Message (Think First, Verify Always), and One Day, are set out in full in Chapter 9, after the evidence.

What We Did

This study integrates data from the federal and state actors profiled in Chapter 6 (which also maps a wider web beyond them) plus an original news corpus:

1. Six years of FBI IC3 data (2020–2025). The FBI’s Internet Crime Complaint Center publishes annual elder fraud reports with state-level victim counts and financial losses across all major crime categories. We compiled, cleaned, and analyzed six years of this data plus the broader IC3 Annual Reports for the same period, spanning 2020 through 2025, from $966 million in 2020 to $7.748 billion in 2025 in reported losses by victims aged 60 and over (with 2021–2025 used as the canonical five-year growth window, +360 percent).

2. The FTC’s Protecting Older Consumers report (December 2025) plus five years of Consumer Sentinel Network Data Books (2020–2024). The Federal Trade Commission’s annual analyses provide the federal government’s most detailed demographic picture of how elder fraud operates, contact methods, payment methods, demographic breakdowns, and the FTC’s $10.1B–$81.5B estimate of the true (underreporting-adjusted) overall cost of fraud to older adults.

3. Seven years of DOJ Elder Abuse Prevention and Prosecution Act (EAPPA) annual reports (2019–2025). The complete federal enforcement record: 283 enforcement actions in 2025 alone, 608 defendants, $2.36 billion stolen across more than one million victims.

4. Seventeen quarters of SSA Office of Inspector General Quarterly Scam Reports (Issues 2–18, July 2021–September 2025). Quarterly granularity on Social Security impersonation scam trends, including the dramatic decline from FY 2019–2021 peak volumes.

5. The CFPB’s Recovering from Elder Financial Exploitation framework (September 2022), the leading federal analysis of what financial recovery actually requires: the four-stage process every victim must navigate, and the Trusted Contact framework this study builds on in Chapter 9.

6. FinCEN advisories, the September 2023 Pig Butchering Alert (FIN-2023-Alert005), the December 2024 FinCEN-impersonation alert (FIN-2024-Alert005), and the 2024 Financial Trend Analysis on Elder Financial Exploitation (documenting $27 billion in related Suspicious Activity Report filings June 2022 – June 2023).

7. The U.S. Secret Service Elder Fraud Advisory (April 2026), the U.S. Postal Inspection Service Annual Reports (FY 2023 and FY 2024), an HHS Office of Inspector General Special Fraud Alert (the March 1998 alert on nursing-home arrangements with hospices, a Medicare provider-side anti-kickback alert), and the U.S. Senate Special Committee on Aging’s Fraud Books (2021, 2023, 2025).

8. An original news corpus of 1,910 articles (August 2025 – May 2026). Beginning in August 2025, we established daily monitoring of news coverage on elder fraud, senior scams, and related topics. Over ten months, this produced 1,910 unique articles from approximately 1,000 distinct news sources. Each article was categorized by scam type, theme, and geography. The corpus drives Chapter 5’s news-analysis findings.

This study’s contribution is to bring those parts together into one picture.

What This Study Is Not

This study is not a government publication. It is an independent nonprofit analysis with an explicit recommendation, not an annual report, designed to stand alone rather than open a series. It is built for this moment: we have aimed for one focused, evidence-led contribution to the public debate.

It is an independent analysis produced by a nonprofit that tracks, analyzes, and explains elder fraud. Our aim is that this problem be understood, measured, and addressed in proportion to its severity.

How to Use This Study

If you are a policymaker: Chapters 1–2 provide the scale. Chapter 7 maps the legislative landscape. Chapter 9 sets out the study’s proposed framework, the Three Ones, built on authority that already exists.

If you are a journalist: Chapter 5 provides a news-media meta-analysis built on 1,910 articles. Chapters 3–4 provide expertise for investigative or explanatory reporting. The state rankings in Chapter 2 provide local angles for every market in America.

If you are a law enforcement professional: Chapter 3 details criminal methods. Chapter 6 maps the full response (the family and community front line, state prosecutors, banks and platforms, and the federal and state agencies) and profiles the enforcement work and partnerships most relevant to your role.

If you are a financial institution: Chapter 1 traces the payment channels the money now moves through (bank transfers and cryptocurrency carry the largest losses) and the $27 billion your industry flagged through Suspicious Activity Reports in a single year of FinCEN review (June 2022 to June 2023). Chapters 3 and 4 detail the scam mechanics your customers face, from the four dominant fraud types to the AI voice-cloning and impersonation tactics now in active use. Chapter 9 proposes the One Message (Think First, Verify Always) for voluntary adoption in customer-facing channels, and a One Day recovery standard.

If you are a caregiver or a family member of an older adult: Chapter 8 explains the human experience of fraud victimization. Chapter 9 presents the Three Ones framework, including the One Message (Think First, Verify Always) we propose for adoption.

If you are a senior: This website and this study were built for you. If a scam happens, a victim may feel ashamed or guilty. Please remember two things. First, former FBI and CIA Director William H. Webster has spoken publicly about being targeted by an elder-fraud scheme; if criminals targeted him, they can target anyone. Second, the person who was scammed is the victim. The blame belongs to the fraudster.

Acknowledgments

This study would not be possible without the public data published by the federal and state sources whose work is documented in the source archive.

The 1,000+ news sources whose journalism informed our analysis, from local television stations to international wire services, provide the daily record of elder fraud.

We acknowledge the individuals whose stories appear in these pages. Sharing one’s experience of fraud requires courage, and their willingness to speak publicly makes prevention possible.

We welcome corrections, challenges, and additions from any reader, government official, researcher, journalist, or citizen. The data in this study is publicly available and our analysis is transparent. If we have made an error, we want to know about it.

Corrections, data submissions, and feedback: [email protected] · https://seniors.hcsk.org

Published June 9, 2026.

Chapter 1: The Numbers We Should Read Together

$7.748 billion, reported stolen from Americans aged 60 and over in 2025. 201,266 complaints. Up 59 percent in a single year, and roughly 360 percent in five.

The Reports America Should Read Together

Every year, multiple federal agencies publish reports on fraud against older Americans. The FBI’s Internet Crime Complaint Center (IC3) releases state-level data on cybercrime victims aged 60 and over. The Federal Trade Commission publishes a broader analysis of consumer fraud through its Sentinel Network. The Treasury Department’s Financial Crimes Enforcement Network (FinCEN) publishes financial-institution suspicious-activity data. The Department of Justice publishes an annual EAPPA Report to Congress documenting federal enforcement. The Consumer Financial Protection Bureau publishes the principal federal framework on what financial recovery actually requires.

All of these reports are public. All are thorough. Reading them together brings an interesting view because each report answers questions the others don’t.

The FBI’s IC3 data tells you where elder fraud is happening. It provides victim counts and dollar losses for every state, broken down by crime type, going back to 2020: granularity no other federal source matches. What it does not capture is the scale of fraud that is never reported to it.

The FTC’s Sentinel data tells you how elder fraud happens, and how much stays hidden. It provides the most detailed picture available of how scammers make contact and how victims pay, broken down by age, and, uniquely among these sources, it estimates the true scale of fraud that goes unreported. What it does not provide is state-level granularity.

The FinCEN SAR data tells you what banks are flagging, independently from victim reports. It corroborates or extends the official complaint data with what financial-institution monitoring detects.

The DOJ’s EAPPA reports tell you what federal prosecutors are doing about it, and what fraction of the documented problem is being met with enforcement (detailed in Chapter 6).

The CFPB’s recovery framework tells you what happens after the loss, and why so little of what is stolen is ever recovered.

This study brings these datasets together into a single picture. What that picture reveals is the subject of this chapter.

Five Years of Escalation

Between 2020 and 2025, the FBI’s Internet Crime Complaint Center recorded elder fraud loss totals that increased more than eightfold, from $966 million in 2020 to $7.748 billion in 2025.

The growth has not been gradual. It has been steep and accelerating.

| Year | Reported Complaints (60+) | Total Losses (60+) | Year-over-Year |

|---|---|---|---|

| 2020 | 105,301 | $966 million | |

| 2021 | 92,371 | $1.685 billion | +74% |

| 2022 | 88,262 | $3.098 billion | +84% |

| 2023 | 101,068 | $3.428 billion | +11% |

| 2024 | 147,127 | $4.885 billion | +43% |

| 2025 | 201,266 | $7.748 billion | +59% |

Source: FBI IC3 Elder Fraud Reports 2020–2023 and IC3 Annual Reports 2024–2025. All categories of elder fraud combined.

Compound growth from 2021 to 2025: approximately +360 percent ($1.685B → $7.748B). Cumulative reported losses over the five years 2021–2025: over $20.8 billion.

The number of reported elder fraud complaints has nearly doubled in this period, rising about 91 percent (from 105,301 in 2020 to 201,266 in 2025). The total dollar losses have increased more than eightfold. And 2025 is the worst year on record by every measure.

The disparity between elder fraud and fraud against younger adults is stark. Adults aged 60 and over accounted for just 20 percent of all IC3 complaints in 2025 but 37 percent of all losses, $7.748 billion out of $20.877 billion (FBI IC3, 2025 Internet Crime Report). Elder fraud losses grew 59 percent year-over-year, compared to 26 percent for all ages combined. Older adults are losing far more than their share of complaints would predict, a pattern consistent with their being targeted for higher-value schemes and with the greater assets many hold.

To put this in perspective: $7.748 billion spread across the 201,266 elder fraud complaints filed in 2025 averages about $38,500 per complaint. That average is pulled sharply upward by a small number of catastrophic losses; 12,444 complainants reported losing more than $100,000. A typical victim loses far less: the FTC puts the median loss for adults 60 and over near $900. And even $38,500 represents only what was reported, a fraction of the true cost.

What the FTC Adds: The Iceberg Beneath the Surface

While the FBI counts internet-related complaints filed with IC3, the FTC collects a broader universe of consumer reports through its Sentinel Network. In 2024, Sentinel received 6.5 million reports from consumers of all ages. Of those, 2.6 million were about fraud, and 1.1 million were about identity theft. Total reported consumer fraud losses across all ages reached $12.8 billion in 2024 (FTC, Protecting Older Consumers 2024-2025, December 2025).

Among consumers aged 60 and over, the FTC documented nearly $2.4 billion in reported losses, up from approximately $600 million in 2020, a 300 percent increase (FTC, Protecting Older Consumers 2024-2025, December 2025).

One of the FTC’s most important contributions to understanding elder fraud is what it estimates goes unreported.

The Reporting Gap

Research the FTC cites finds that just 4.8 percent of fraud victims report their experience to a government entity or the Better Business Bureau. Reporting rates vary dramatically by loss amount:

- 2.0 percent of victims who lost under $1,000 file a report

- 6.7 percent of victims who lost over $1,000 file a report

Even among those who do report, the oldest and most vulnerable victims often rely on others to do so. For adults aged 80 and over, 16 percent of fraud reports were filed by a third party (an adult child, spouse, or caregiver), the highest rate of any age group. The median loss in those third-party reports was $6,000, nearly four times the $1,650 overall median for that age group. This suggests that cases severe enough to come to a family member’s attention involve substantially more money than what victims report on their own.

Yet the reporting data also reveals an important counternarrative: 74 percent of fraud reports filed by older adults indicated no monetary loss. Adults 60 and over were 62 percent more likely than younger adults to file a no-loss report, meaning they recognized the scam and reported it without losing money. Older Americans are not, as stereotype suggests, uniformly vulnerable. Many are vigilant and report fraud attempts even when they do not lose a cent. The crisis is not that seniors cannot detect fraud, it is that when fraud succeeds, the consequences are catastrophic.

Using these reporting rates to extrapolate from actual Sentinel data, the FTC estimates the true cost of fraud to older adults in 2024 falls between:

- $10.1 billion (conservative, assuming everyone who lost $10,000 or more reported)

- $81.5 billion (full extrapolation using research-based reporting rates)

Even the conservative estimate, $10.1 billion, is more than four times what older victims reported to the FTC ($2.4 billion). The $2.4 billion older adults reported is only about one-quarter of the FTC’s most conservative true-cost estimate ($10.1 billion), and a far smaller share of its full research-based extrapolation ($81.5 billion). FinCEN’s $27 billion in bank-flagged suspicious activity over a comparable period, discussed below, points the same way: the reported totals capture only a fraction of true losses.

The FinCEN Confirmation

A third federal data source corroborates the FTC’s estimates, and suggests they may still be conservative.

The Treasury Department’s FinCEN tracks Bank Secrecy Act (BSA) reports, predominantly Suspicious Activity Reports (SARs), filed by banks and financial institutions. Per FinCEN’s Financial Trend Analysis: Elder Financial Exploitation (April 2024), between June 15, 2022 and June 15, 2023, financial institutions filed 155,415 elder-financial-exploitation reports worth more than $27 billion under the Bank Secrecy Act (banks accounted for 72 percent of those filings).

This figure represents what financial institutions flag as suspicious, not what victims report or what law enforcement investigates, but what automated monitoring systems and trained bank employees identify as potentially fraudulent activity involving older adults. Because it is bank-flagged suspicious activity rather than completed, adjudicated loss, FinCEN cautions it may include attempted as well as duplicate transactions, so it is not a dollar-for-dollar match with the FBI’s reported losses. Even so, it shows banking-side detection registering fraud on a scale several times larger than the complaint data captures.

The CFPB Recovery Gap

A fourth federal data source completes the picture, by documenting what happens after the loss.

The FBI’s Recovery Asset Team is the federal government’s primary tool for clawing stolen funds back, and where it can act, it works: in the 642 elder-fraud cases reported fast enough for it to step in, it froze about half the money at risk ($32.9 million of $65.4 million). The limit is not the team’s effectiveness but the system’s reach. Only those 642 cases, out of 201,266 elder fraud complaints, reached the freeze window in time, so of the $7.748 billion lost by older Americans, less than half of one percent was frozen. The Consumer Financial Protection Bureau’s Recovering from Elder Financial Exploitation: A Framework for Policy and Research (September 2022) traces this to a four-stage process every victim must navigate, from identification to reporting to investigation to the eventual return of funds, with different actors at each stage and no automatic handoff between them. Once a fraudulent transfer clears, the money is almost always gone.

Four federal data sources point the same way: the FBI’s more-than-eightfold growth in reported losses, the FTC’s iceberg estimate of unreported losses, FinCEN’s banking-side detection of suspect activity, and the CFPB’s documentation of post-loss recovery. Together they confirm one conclusion: the scale of elder fraud is enormous, the visible figure is a small fraction of the true total, and only a fraction of what is stolen is recovered.

What This Means in Human Terms

Research the FTC cites finds that only about 1 in 20 fraud victims ever files a report. The FBI and FTC count fraud through different channels, so no precise headcount is possible. But if anything close to those reporting rates holds, the roughly 200,000 elder complaints the FBI logged in 2025 represent only a fraction of true victims, a rough signal that the real number runs into the millions, not the hundreds of thousands.

Each number represents a person, typically someone over 60, often living alone, frequently losing a significant portion of their retirement savings to a criminal who, in the vast majority of cases, is never identified or held to account.

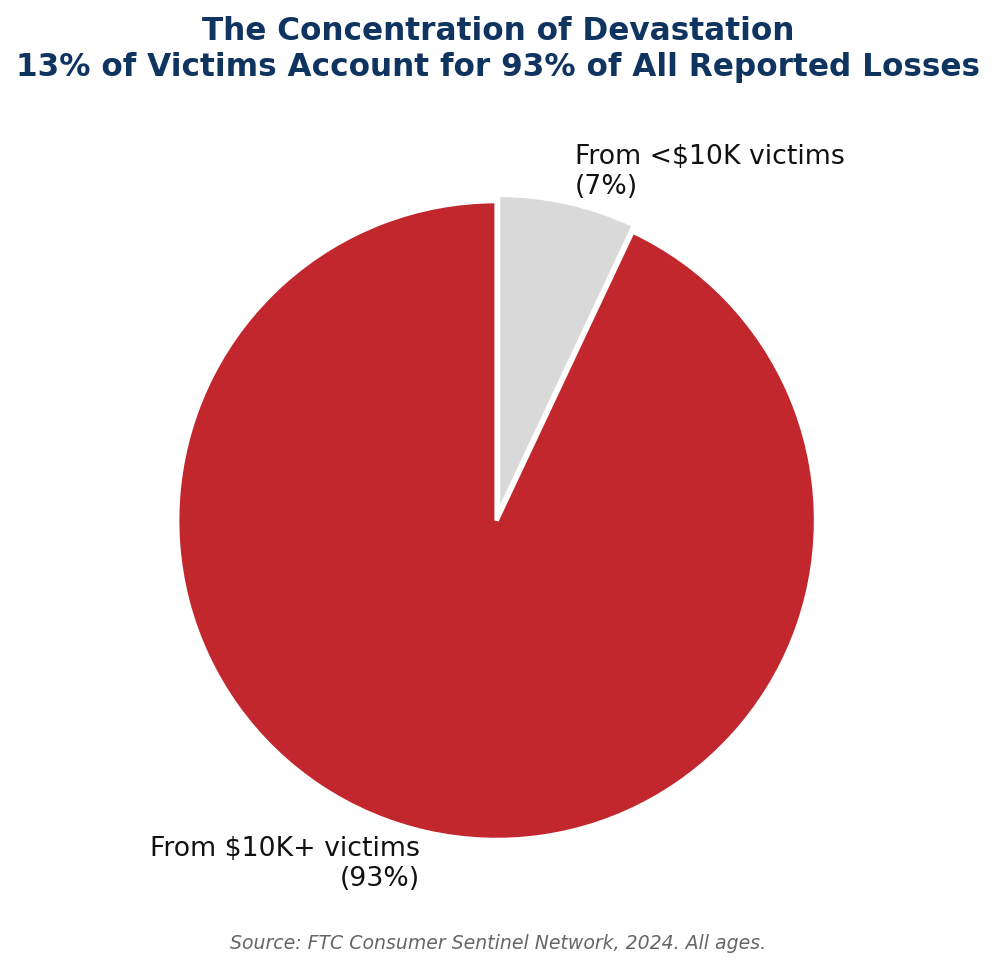

The Concentration of Devastation

One of the most striking findings from the FTC data is how concentrated the financial damage is among a relatively small number of high-loss victims.

In 2024, across all ages, just 13 percent of consumers who reported a fraud loss lost $10,000 or more, yet their combined losses equaled 93 percent of all reported losses to the FTC’s Sentinel Network. The number of older adults reporting losses over $100,000 has increased 351 percent since 2020, from 1,136 reports in 2020 to 5,125 in 2024. Reports in the $10,000–$100,000 tier also rose sharply, nearly tripling, from 6,965 to 19,679 (a 183 percent increase).

The FBI’s IC3 data corroborates this concentration pattern. In 2025, the average loss per elder fraud complaint was $38,500, but this average masks enormous variance. Of the 201,266 elder complaints filed that year, 12,444 complainants reported losses exceeding $100,000. These high-loss victims, roughly six percent of all elder complainants, account for a disproportionate share of the $7.748 billion total.

These are not people losing $50 to a phishing email. These are retirees losing $200,000 to an investment scam. Widows wiring $75,000 to someone impersonating the FTC. Grandfathers handing $30,000 in cash to a courier they believe was sent by their bank.

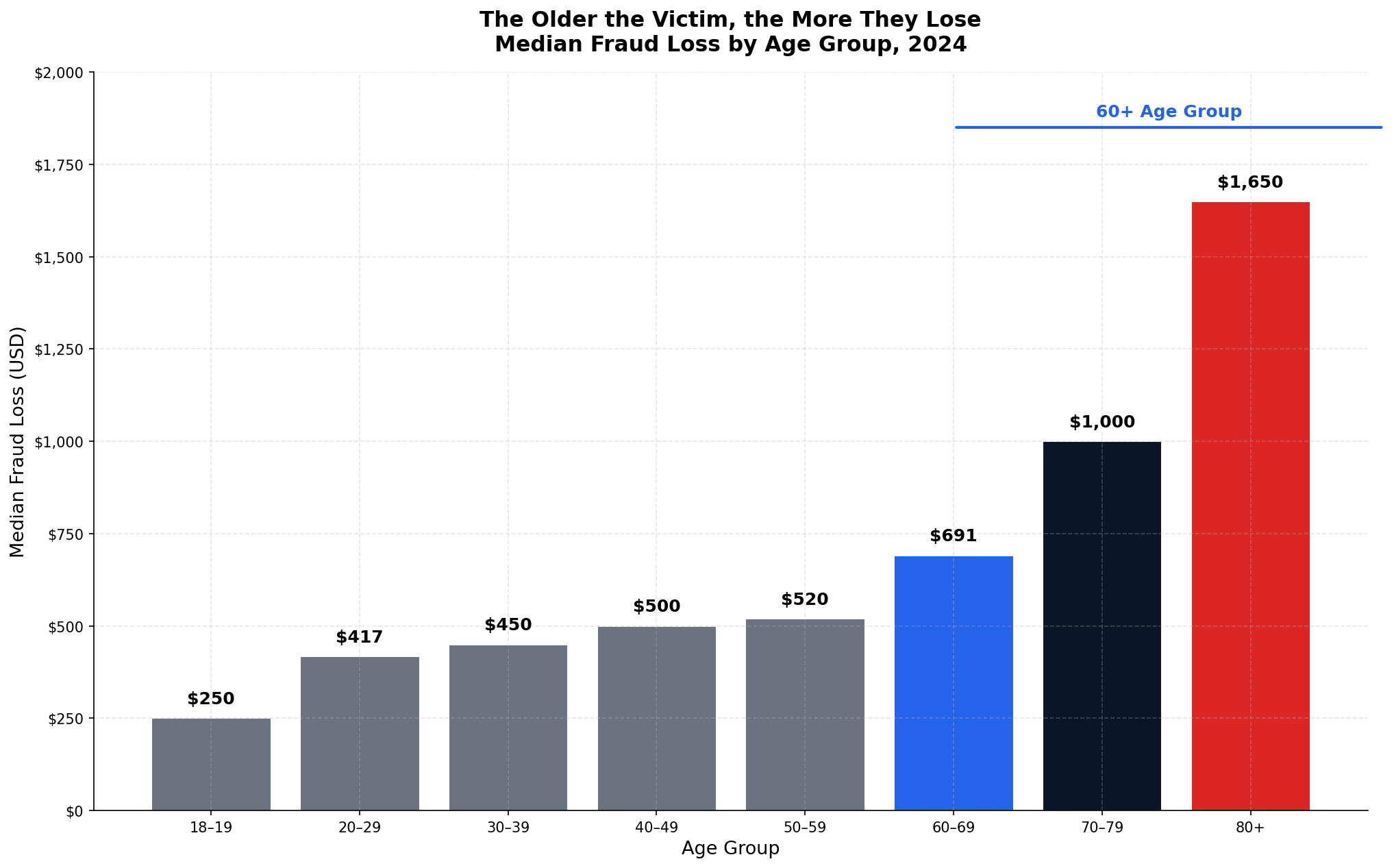

The combined median loss for all adults 60 and over was $900 in 2024, up 38 percent from $650 the year before (FTC, Protecting Older Consumers 2024-2025). And the median rises sharply with age. The median loss for Americans aged 80 and over was $1,650 in 2024, far higher than any other age group. For those aged 70–79, the median was $1,000. For those aged 60–69, it was $691.

The older the victim, the more they lose.

How Scammers Make Contact

The FTC’s Sentinel data reveals a critical shift in how scammers reach their victims, and it differs significantly by age group.

Social Media: The New Vector

In 2024, social media surpassed all other contact methods as the leading source of elder fraud by total reported losses. Older adults reported $561 million in losses from fraud initiated on social media platforms, a 44 percent increase from the previous year, with the median social media loss surging 91 percent year-over-year to $650. Losses to social-media-initiated fraud have increased nearly ninefold since 2020.

The highest aggregate losses from fraud that started on social media were on investment scams (51 percent of social-media-initiated losses) and romance scams (28 percent). By number of loss reports, however, the most common social-media fraud older adults reported was online shopping scams (31 percent).

Phone Calls: Highest Loss Per Victim

While social media generates more aggregate losses, phone calls remain the costliest contact method per victim: the $2,210 median loss is the highest of any channel the FTC tracks, more than three times the $650 median for social media fraud.

This disparity reflects the different nature of phone-based scams: they typically involve high-pressure impersonation of government agencies or financial institutions, targeting victims who are less active online but highly responsive to authoritative-sounding callers.

For Americans aged 80 and over, phone calls remain the dominant contact method by both total losses and number of reports, with social media a distant second.

| Contact Method | Total Losses (60+) | Change from 2023 | Median Loss |

|---|---|---|---|

| Social Media | $561M | +44% | $650 |

| Phone Call | $502M | +24% | $2,210 |

| Website or App | $303M | +45% | $272 |

| Text Message | $183M | +41% | $1,560 |

| Online Ad/Pop-up | $147M | +24% | $288 |

| $143M | +14% | $1,000 |

Source: FTC Consumer Sentinel Network, 2024. Adults aged 60 and over.

How Victims Pay: The Money Trail

Understanding how stolen money moves is essential for both prevention and recovery. The FTC data reveals that the most expensive payment methods for older adults are not the most commonly reported, a distinction with important implications.

Bank Transfers and Cryptocurrency: Where the Big Money Goes

Bank transfers accounted for the highest total losses by older adults at $832 million (up 24 percent from 2023), followed by cryptocurrency at $454 million (up 15 percent). Together, bank transfers and cryptocurrency were the two costliest payment methods for older adults, about $1.29 billion in losses, more than half of the nearly $2.4 billion older adults reported losing to the FTC in 2024.

Since 2020, elder fraud losses involving bank transfers have increased eightfold. Losses involving cryptocurrency have increased twentyfold. The broader IC3 data underscores cryptocurrency’s dominance: total cryptocurrency fraud across all ages reached $11.4 billion from 181,565 complaints in 2025, making it the single highest-loss descriptor in IC3’s 2025 all-ages data (cryptocurrency is a payment-method descriptor that spans multiple crime types, not a standalone crime category). Adults 60 and over bear a disproportionate share: 38 percent of all cryptocurrency losses ($4.35 billion, the IC3’s combined Cryptocurrency and Cryptocurrency Wallet descriptor).

Gift Cards and Credit Cards: Most Frequently Reported

Despite generating lower total losses, credit cards (26 percent of loss reports) and gift cards (16 percent) were the payment methods most frequently reported by older adults. Gift cards remain the signature payment method for government impersonation scams, tech support scams, romance scams, and family impersonation scams.

| Payment Method | Total Losses (60+) | Change from 2023 | Share of Reports |

|---|---|---|---|

| Bank Transfer | $832M | +24% | 11% |

| Cryptocurrency | $454M | +15% | 10% |

| Cash | $156M | +57% | 4% |

| Gift Card | $124M | +5% | 16% |

| Check | $121M | +19% | 3% |

| Wire Transfer | $105M | -16% | 3% |

| Credit Card | $77M | +33% | 26% |

| Payment App | $80M | +156% | 14% |

Source: FTC Consumer Sentinel Network, 2024. Adults aged 60 and over.

The rise of payment apps (+156 percent) and cash payments (+57 percent) signals that scammers are constantly adapting to evade fraud detection systems built around traditional wire transfers. Payment apps and money-transfer services, the kind used to send money directly to another person, were cited in 90,571 fraud reports across all ages in 2024, with losses totaling $391 million.

For older adults, the rapid adoption of payment apps combined with limited understanding of their irrevocable nature, has created a new vulnerability that did not exist five years ago.

The Combined Picture

When the FBI’s state-level data, the FTC’s national demographic data, FinCEN’s banking-side detection data, and the CFPB’s recovery-process documentation are read together, the same picture emerges from every angle:

1. The problem is growing faster than any response. Annual reported losses for the 60+ age group have grown from $1.685 billion (2021) to $7.748 billion (2025), approximately +360 percent in five years.

2. Reported numbers dramatically understate reality. With fewer than one in twenty frauds reported, the true number of elder fraud victims likely runs several times higher than the reported count, into the millions per year on an order-of-magnitude basis, since the FBI and FTC count through different channels. The true annual cost is likely several times higher than what is reported, consistent with the FTC’s wide underreporting estimate.

3. The channels of attack are shifting. Social media has overtaken phone calls as the leading contact method for elder fraud by total losses. Cryptocurrency and bank transfers have replaced gift cards as the principal money-moving channels. The infrastructure of the threat is moving faster than the infrastructure of the response.

4. Recovery depends on speed, and most cases do not reach the freeze window in time. In 2025 the FBI froze about half the money in the few hundred cases reported fast enough to act, but the system reached that freeze window in fewer than one in three hundred cases, so less than half of one percent of the dollars stolen from older Americans was frozen.

The Three Findings

The data presented in this chapter, five years of FBI growth, FTC underreporting, FinCEN’s banking detection, and the FBI’s own recovery results, points consistently in one direction. The visible scale of the problem is large and growing. The hidden scale is several times larger still. And the money, once gone, is almost never recovered: in 2025 less than half of one percent of it was frozen in time, not for want of an effective tool but because almost no case reached that tool fast enough:

- No single front door, ten federal actors, most with their own separate intake channels, and a scatter of federal reporting sites, plus 50+ state portals, with no single number to call and no designated first-click destination

- Inconsistent protective messaging, taglines borrowed from cybersecurity that do not address the manipulation-based threat model documented in the FTC’s research

- Speed mismatch, the FBI’s Recovery Asset Team can freeze a fraudulent wire only when it is reported almost immediately

America has the people, the agencies, the laws, and the data. What it does not yet have is a way to connect them, the coordination and simplification that Chapter 9 takes up.

In the next chapter, we examine where in America elder fraud losses are most severe, ranking the 50 states, the District of Columbia, and Puerto Rico by losses, per-capita impact, and five-year growth trajectory.

Data Sources for Chapter 1:

- FBI Internet Crime Complaint Center (IC3), Elder Fraud Annual Reports, 2020–2023

- FBI IC3, 2024 Internet Crime Report and 2025 Internet Crime Report

- Federal Trade Commission, Protecting Older Consumers 2024-2025, December 1, 2025

- Federal Trade Commission, Consumer Sentinel Network Data Book 2024, March 2025

- Federal Trade Commission, Consumer Sentinel Network Data Books 2020-2023

- U.S. Treasury FinCEN, Financial Trend Analysis: Elder Financial Exploitation, April 2024

- Consumer Financial Protection Bureau, Recovering from Elder Financial Exploitation: A Framework for Policy and Research, September 2022

Chapter 2: State-by-State Rankings

Elder fraud is a national crisis, but it does not strike every state equally.

The Map of Loss

In 2025, elder fraud reached every corner of the United States. All 50 states, the District of Columbia, and Puerto Rico, the 52 reporting jurisdictions in FBI IC3 state-level data, recorded victims and financial losses. But the distribution of those losses reveals a geography of vulnerability that challenges simple assumptions about who is most at risk and why.

This chapter presents four distinct rankings. Each tells a different story:

- Total losses, which states bear the greatest aggregate financial burden

- Per-capita losses (loss per older resident), which states show the highest reported losses per senior

- Five-year growth rate, where the problem is accelerating fastest

- Cadence of harm (how often an older adult is scammed), which states see victims most frequently

Understanding all four is essential. A state can rank low in total losses but high in growth rate, signaling a crisis in its early stages. A state with moderate totals may have devastating per-capita numbers because its senior population is small. Policymakers and journalists who rely on a single ranking miss the full picture.

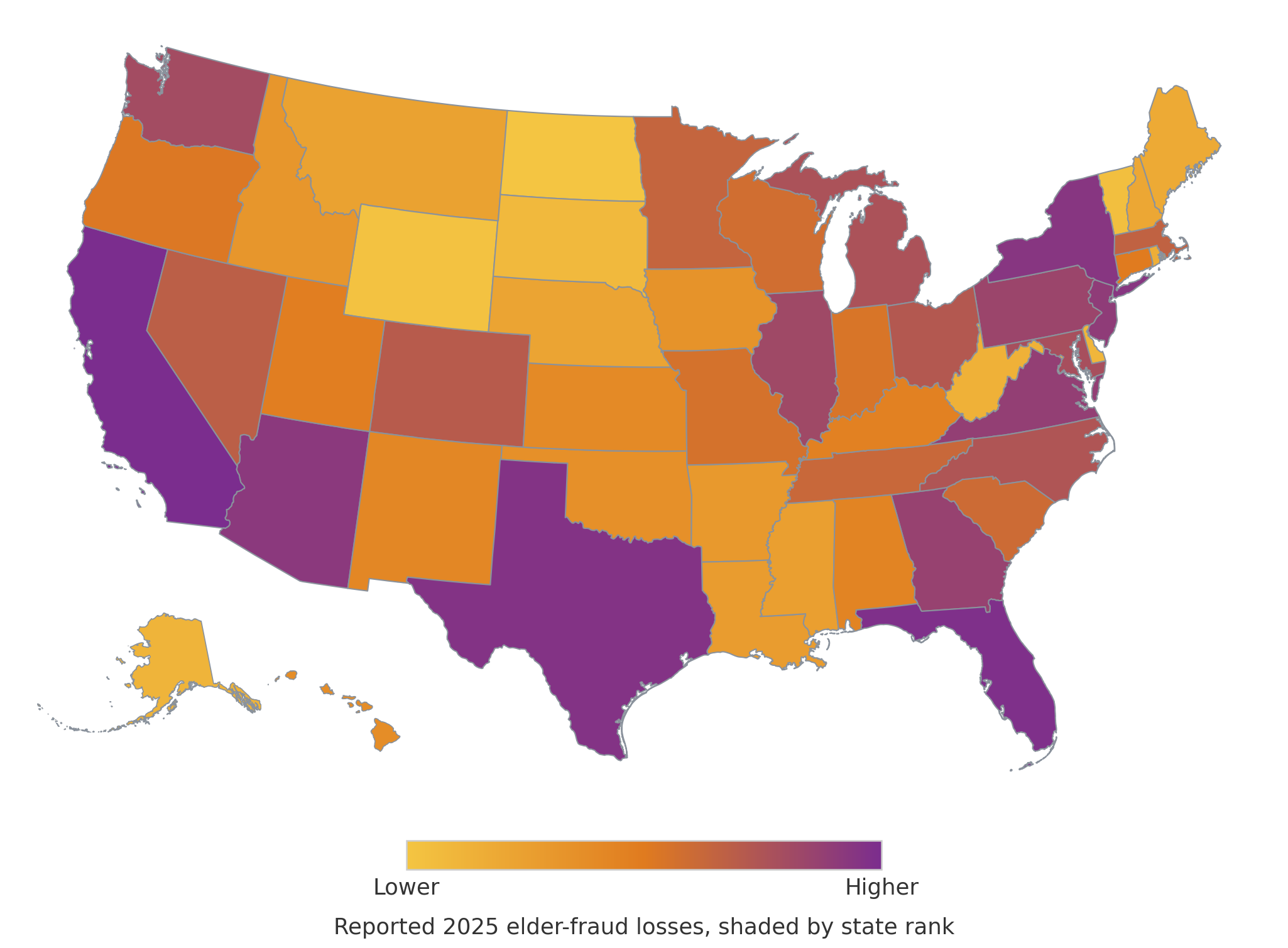

The map shows that geography at a glance, built from the same state-loss data as the report’s cover.

The geography of loss: reported 2025 elder-fraud losses by state (FBI IC3; four major scam categories; victims aged 60+). States are shaded by their rank on total reported losses, lighter for lower and darker for higher, as the color key shows; the exact state-by-state figures appear in the rankings that follow.

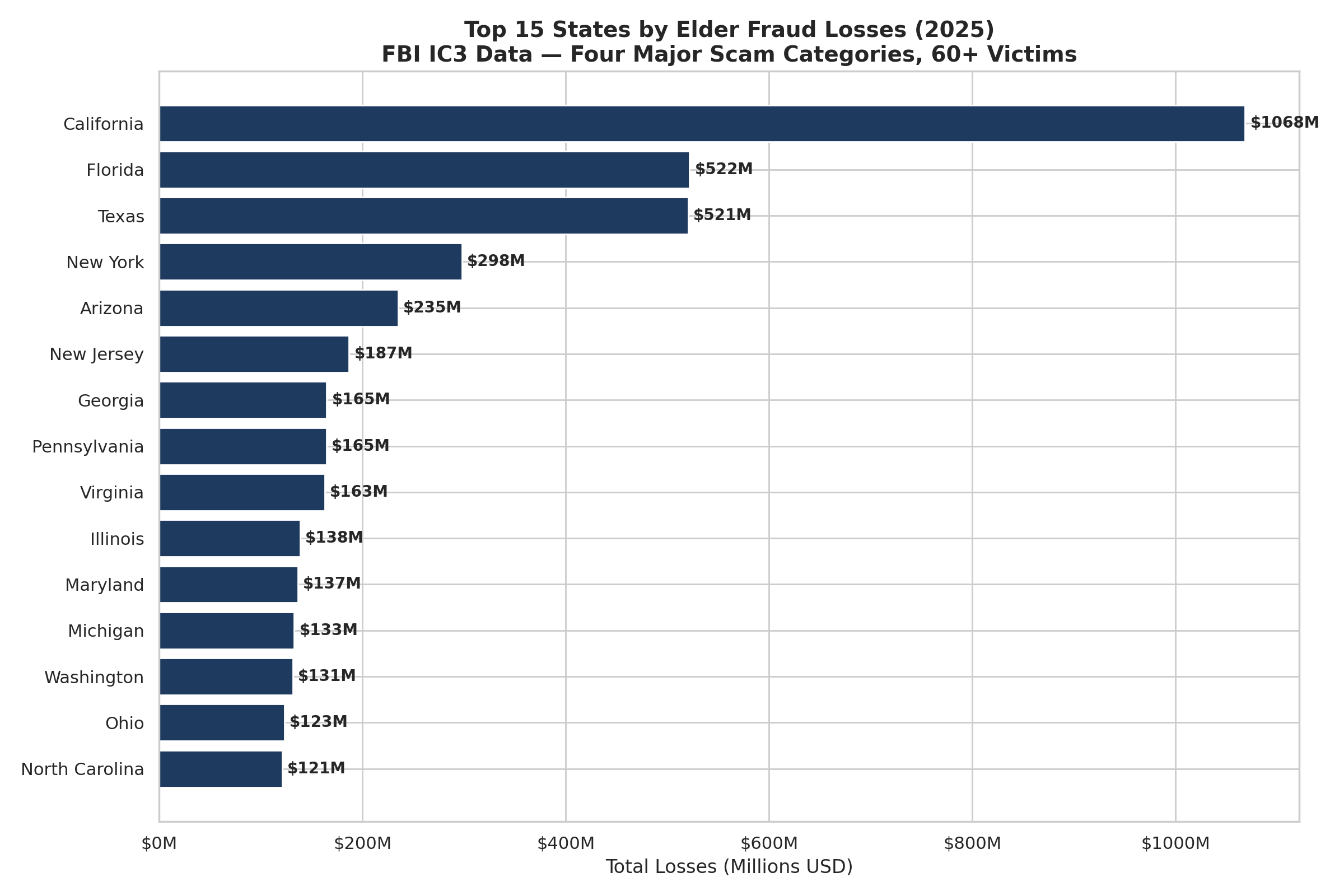

Ranking 1: Total Losses by State (2025)

California led the nation in elder fraud losses by a wide margin, with $1.068 billion, just over double the second-ranked state. Florida and Texas were separated by less than $2 million.

The top ten states accounted for $3.46 billion, or 63% of all reported losses across the four scam categories tracked in this ranking (investment, tech support, romance, and government impersonation). The bottom ten accounted for just $90 million. (All-crime-type state totals run higher: California’s all-type total is $1.404 billion versus $1.068 billion across these four categories.)

Top 15 states by elder fraud losses, 2025. Source: FBI IC3 state-level files, four major scam categories, victims aged 60+.

Complete State Ranking by Total Losses (2025)

| Rank | State | Total Losses | Victims | 5-Year Growth |

|---|---|---|---|---|

| 1 | California | $1,068.3M | 7,987 | +481% |

| 2 | Florida | $521.7M | 5,847 | +433% |

| 3 | Texas | $520.5M | 5,087 | +612% |

| 4 | New York | $297.7M | 3,034 | +369% |

| 5 | Arizona | $234.8M | 3,402 | +745% |

| 6 | New Jersey | $186.8M | 1,546 | +389% |

| 7 | Georgia | $164.7M | 1,677 | +1,101% |

| 8 | Pennsylvania | $164.6M | 2,221 | +381% |

| 9 | Virginia | $162.9M | 1,799 | +393% |

| 10 | Illinois | $138.4M | 1,919 | +512% |

| 11 | Maryland | $136.5M | 1,189 | +691% |

| 12 | Michigan | $132.8M | 1,554 | +786% |

| 13 | Washington | $131.5M | 1,644 | +518% |

| 14 | Ohio | $123.1M | 1,800 | +632% |

| 15 | North Carolina | $120.7M | 1,763 | +571% |

| 16 | Colorado | $103.1M | 1,225 | +416% |

| 17 | Massachusetts | $81.0M | 1,173 | +343% |

| 18 | Tennessee | $77.6M | 1,124 | +397% |

| 19 | Minnesota | $77.0M | 850 | +624% |

| 20 | South Carolina | $72.6M | 1,050 | +690% |

| 21 | Nevada | $71.5M | 1,082 | +178% |

| 22 | Missouri | $70.0M | 1,216 | +764% |

| 23 | Wisconsin | $67.9M | 927 | +563% |

| 24 | Indiana | $59.8M | 1,054 | +540% |

| 25 | Oregon | $58.3M | 1,078 | +428% |

| 26 | Kentucky | $53.0M | 728 | +535% |

| 27 | Utah | $52.1M | 613 | +527% |

| 28 | Hawaii | $48.1M | 394 | +677% |

| 29 | Connecticut | $47.4M | 659 | +683% |

| 30 | New Mexico | $43.6M | 560 | +1,537% |

| 31 | Kansas | $43.6M | 502 | +743% |

| 32 | Alabama | $43.6M | 769 | +498% |

| 33 | Oklahoma | $39.3M | 738 | +729% |

| 34 | Idaho | $28.7M | 437 | +1,305% |

| 35 | Louisiana | $26.6M | 645 | +114% |

| 36 | Montana | $25.7M | 251 | +1,214% |

| 37 | Iowa | $25.6M | 419 | +678% |

| 38 | Arkansas | $23.7M | 599 | +1,235% |

| 39 | Nebraska | $23.1M | 335 | +1,276% |

| 40 | Mississippi | $22.7M | 349 | +568% |

| 41 | New Hampshire | $19.0M | 307 | +2,247% |

| 42 | Maine | $17.8M | 253 | +1,449% |

| 43 | West Virginia | $14.7M | 330 | +748% |

| 44 | Delaware | $12.9M | 225 | +331% |

| 45 | Alaska | $12.6M | 231 | +260% |

| 46 | South Dakota | $12.4M | 146 | +682% |

| 47 | Rhode Island | $11.8M | 172 | +234% |

| 48 | District of Columbia | $7.6M | 94 | +527% |

| 49 | Vermont | $6.8M | 133 | +158% |

| 50 | Puerto Rico | $4.4M | 154 | +216% |

| 51 | Wyoming | $3.6M | 126 | +12% |

| 52 | North Dakota | $3.3M | 87 | +286% |

Source: FBI IC3 Elder Fraud Reports, 2021–2025. Four major scam categories, victims aged 60+.

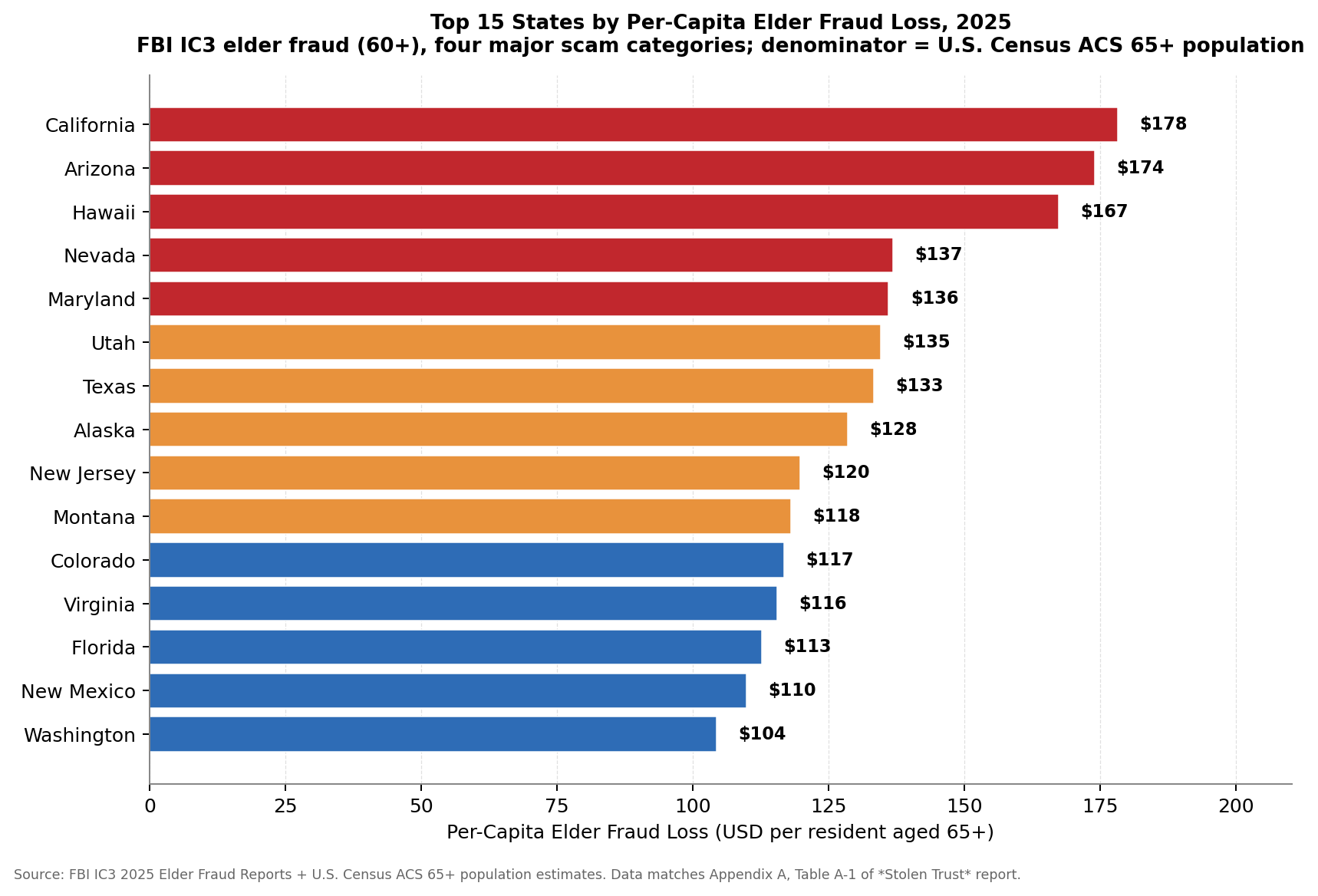

Ranking 2: Per-Capita Losses, Adjusting for Population

Total loss rankings inevitably favor large states. California, with nearly 6 million residents over 65, will generate more fraud reports than Montana, with 220,000.

The per-capita ranking produces some surprises.

Top 10 States by Reported Losses Per Older Resident (2025)

| Per-Capita Rank | State | Loss Per Senior | Total Losses | Total Loss Rank |

|---|---|---|---|---|

| 1 | California | $178 | $1,068M | 1 |

| 2 | Arizona | $174 | $235M | 5 |

| 3 | Hawaii | $167 | $48M | 28 |

| 4 | Nevada | $137 | $72M | 21 |

| 5 | Maryland | $136 | $137M | 11 |

| 6 | Utah | $135 | $52M | 27 |

| 7 | Texas | $133 | $521M | 3 |

| 8 | Alaska | $128 | $13M | 45 |

| 9 | New Jersey | $120 | $187M | 6 |

| 10 | Montana | $118 | $26M | 36 |

Hawaii, ranked only 28th in total losses, jumps to 3rd highest per capita, at $167 per senior. Utah, 27th in total losses, rises to 6th, and Alaska, 45th in total losses, to 8th per capita. Montana, 36th in total losses, reaches 10th per capita.

These are states where fewer seniors live, but those who do face disproportionate risk. Per-capita numbers reveal where reported losses per senior are highest, a better proxy for individual exposure than state totals.

Bottom 5: Lowest Reported Losses Per Older Resident

| Per-Capita Rank | State | Loss Per Senior | Total Losses |

|---|---|---|---|

| 48 | West Virginia | $40 | $14.7M |

| 49 | Louisiana | $35 | $26.6M |

| 50 | Wyoming | $34 | $3.6M |

| 51 | North Dakota | $26 | $3.3M |

| 52 | Puerto Rico | $6 | $4.4M |

Per-capita figures divide reported four-category losses by each jurisdiction’s residents aged 65 and over, using U.S. Census Bureau American Community Survey estimates (2019–2023), an external dataset; see Data Sources. ACS publishes a standard 65-and-over older-adult denominator used consistently across all jurisdictions, so these figures are best read as a normalized state-to-state comparison rather than a literal loss-per-60+-resident calculation.

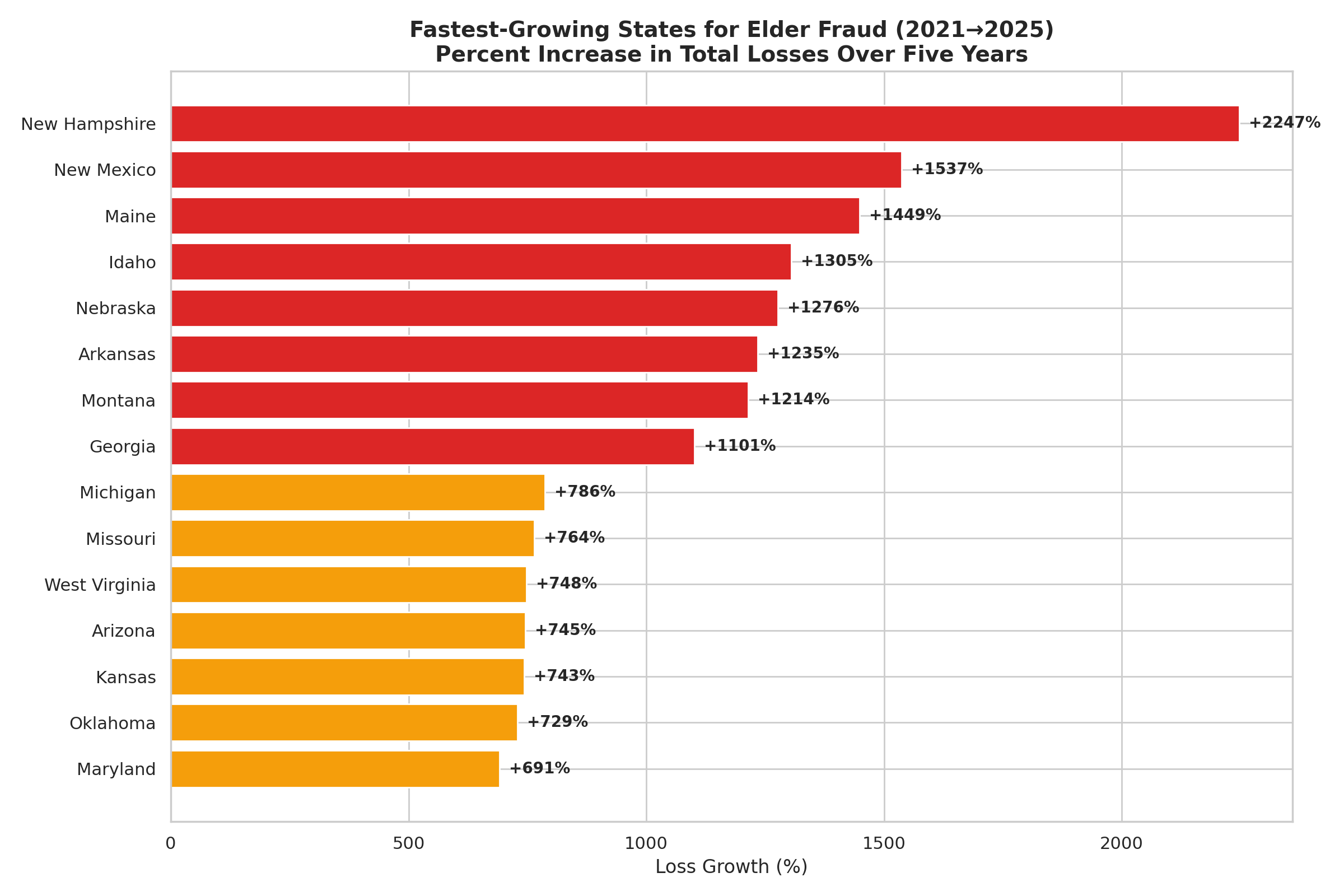

Ranking 3: Where the Crisis Is Accelerating

The five-year growth rate shows the widest variation of the four rankings. While every state has seen elder fraud increase since 2021, the rate of acceleration varies enormously, from Wyoming’s 12 percent increase to New Hampshire’s 2,247 percent.

Fastest-growing states for elder fraud, 2021 to 2025 five-year growth. Source: FBI IC3 state-level files, four major scam categories.

Top 15 Fastest-Growing States (2021 → 2025)

| Rank | State | 2021 Losses | 2025 Losses | Growth |

|---|---|---|---|---|

| 1 | New Hampshire | $0.8M | $19.0M | +2,247% |

| 2 | New Mexico | $2.7M | $43.6M | +1,537% |

| 3 | Maine | $1.1M | $17.8M | +1,449% |

| 4 | Idaho | $2.0M | $28.7M | +1,305% |

| 5 | Nebraska | $1.7M | $23.1M | +1,276% |

| 6 | Arkansas | $1.8M | $23.7M | +1,235% |

| 7 | Montana | $2.0M | $25.7M | +1,214% |

| 8 | Georgia | $13.7M | $164.7M | +1,101% |

| 9 | Michigan | $15.0M | $132.8M | +786% |

| 10 | Missouri | $8.1M | $70.0M | +764% |

| 11 | West Virginia | $1.7M | $14.7M | +748% |

| 12 | Arizona | $27.8M | $234.8M | +745% |

| 13 | Kansas | $5.2M | $43.6M | +743% |

| 14 | Oklahoma | $4.7M | $39.3M | +729% |

| 15 | Maryland | $17.3M | $136.5M | +691% |

A pattern emerges in this data: the states growing fastest are smaller, less-populous states. New Hampshire, Maine, Idaho, Montana, Nebraska, Arkansas, these are not the states that dominate headlines about cybercrime. Yet these states post some of the highest elder-fraud growth rates in the nation. New Hampshire’s reported losses in these four categories rose 2,247% over five years, for example, against roughly 360% growth in the nationwide all-category elder-fraud total. The two figures sit on different bases, one state’s four tracked categories versus the national all-category total, and New Hampshire’s percentage is amplified by its very small 2021 starting point of $0.8 million, but the underlying jump from $0.8 million to $19.0 million is real.

One possible explanation is that elder fraud is no longer concentrated in large metro areas: as more seniors in smaller states and rural areas come online, they face the same threats, often with thinner local support to fall back on. The loss data in this report cannot confirm that mechanism; what it does show is that loss growth is now steepest in smaller, less-populous states, exactly the places where coordinated scam-awareness and victim-services resources can be hardest to reach.

Georgia is the only state to rank in the top ten for both total losses (7th) and five-year growth (8th). Its losses grew twelvefold, from $13.7 million in 2021 to $164.7 million in 2025. That combination of scale and acceleration makes Georgia notable for ranking high on both measures at once.

Ranking 4: The Cadence of Harm

Behind every state-level loss total is a victim count, and behind every victim count is a cadence. How often is an older adult, in a given state, being scammed online?

The answer in California is every 66 minutes. In Florida, every 90 minutes. In Texas, every 1.7 hours. In Arizona, every 2.6 hours. In New York, every 2.9 hours. In Pennsylvania, every 3.9 hours. In Illinois, Virginia, Ohio, and North Carolina, every 4 to 5 hours. Even in the smallest, lowest-loss reporting jurisdictions, the cadence is not “rare”: in North Dakota and the District of Columbia, an older adult is scammed online every four days; in Wyoming, every 2.9 days; in Vermont, every 2.7 days.

These counts include reported victims only. Research the FTC cites finds that just 4.8 percent of fraud victims report the incident to a government entity or the Better Business Bureau, so true victim counts, and the true cadence, are several times higher.

The table below shows the FBI IC3 2025 four-category victim cadence for all 52 reporting jurisdictions, sorted by 2025 rank:

| Rank | State | 2025 victims | An older adult is scammed online… |

|---|---|---|---|

| 1 | California | 7,987 | every 66 minutes |

| 2 | Florida | 5,847 | every 90 minutes |

| 3 | Texas | 5,087 | every 1.7 hours |

| 4 | New York | 3,034 | every 2.9 hours |

| 5 | Arizona | 3,402 | every 2.6 hours |

| 6 | New Jersey | 1,546 | every 5.7 hours |

| 7 | Georgia | 1,677 | every 5.2 hours |

| 8 | Pennsylvania | 2,221 | every 3.9 hours |

| 9 | Virginia | 1,799 | every 4.9 hours |

| 10 | Illinois | 1,919 | every 4.6 hours |

| 11 | Maryland | 1,189 | every 7 hours |

| 12 | Michigan | 1,554 | every 5.6 hours |

| 13 | Washington | 1,644 | every 5.3 hours |

| 14 | Ohio | 1,800 | every 4.9 hours |

| 15 | North Carolina | 1,763 | every 5 hours |

| 16 | Colorado | 1,225 | every 7 hours |

| 17 | Massachusetts | 1,173 | every 7 hours |

| 18 | Tennessee | 1,124 | every 8 hours |

| 19 | Minnesota | 850 | every 10 hours |

| 20 | South Carolina | 1,050 | every 8 hours |

| 21 | Nevada | 1,082 | every 8 hours |

| 22 | Missouri | 1,216 | every 7 hours |

| 23 | Wisconsin | 927 | every 9 hours |

| 24 | Indiana | 1,054 | every 8 hours |

| 25 | Oregon | 1,078 | every 8 hours |

| 26 | Kentucky | 728 | every 12 hours |

| 27 | Utah | 613 | every 14 hours |

| 28 | Hawaii | 394 | every 22 hours |

| 29 | Connecticut | 659 | every 13 hours |

| 30 | New Mexico | 560 | every 16 hours |

| 31 | Kansas | 502 | every 17 hours |

| 32 | Alabama | 769 | every 11 hours |

| 33 | Oklahoma | 738 | every 12 hours |

| 34 | Idaho | 437 | every 20 hours |

| 35 | Louisiana | 645 | every 14 hours |

| 36 | Montana | 251 | every 1.5 days |

| 37 | Iowa | 419 | every 21 hours |

| 38 | Arkansas | 599 | every 15 hours |

| 39 | Nebraska | 335 | every 26 hours |

| 40 | Mississippi | 349 | every 25 hours |

| 41 | New Hampshire | 307 | every 29 hours |

| 42 | Maine | 253 | every 1.4 days |

| 43 | West Virginia | 330 | every 27 hours |

| 44 | Delaware | 225 | every 1.6 days |

| 45 | Alaska | 231 | every 1.6 days |

| 46 | South Dakota | 146 | every 2.5 days |

| 47 | Rhode Island | 172 | every 2.1 days |

| 48 | District of Columbia | 94 | every 4 days |

| 49 | Vermont | 133 | every 2.7 days |

| 50 | Puerto Rico | 154 | every 2.4 days |

| 51 | Wyoming | 126 | every 2.9 days |

| 52 | North Dakota | 87 | every 4 days |

Source: HCSK computation, based on the FBI IC3 Elder Fraud Report, 2025 (victims aged 60+, four major scam categories: investment, tech support, romance, government impersonation). Cadence = 525,600 minutes per year ÷ 2025 reported victim count, rounded.

For the high-loss states (California, Florida, Texas, Arizona, New York), the cadence is a matter of minutes or a few hours. For mid-sized states, it is several hours to half a day. For the smallest states and territories, it is days. No reporting jurisdiction’s cadence is “rarely”. Whether someone lives in Los Angeles or Bismarck, frauds arrive often enough that nearly every community will see one. That is why the cadence of harm puts steady pressure on the systems around an older adult: family, bank, police, and agency hotlines.

In the largest states, the next reported victim is, on average, less than two hours away. Chapter 9 returns to what that cadence implies for response timing.

Regional Patterns

When viewed by region, distinct patterns emerge:

Sun Belt states (Arizona, Florida, Texas, Nevada) rank high on at least one of total or per-capita losses; Arizona and Texas rank high on both, while Nevada is driven by per-capita risk and Florida by aggregate scale. Large retiree populations, high average wealth, and extensive internet connectivity create a target-rich environment.

Mountain West states such as Montana, Idaho, and New Mexico show among the highest growth rates but relatively low total losses, for now. These may be states where the crisis is still in its early stages.

Northeast states (New York, New Jersey, Massachusetts) show high total losses but below-median five-year growth (343 to 389 percent versus a 52-jurisdiction median of 551 percent), consistent with a fraud problem that scaled earlier rather than recently. Connecticut is an exception within the region, with above-median growth (683 percent).

Deep South states (Louisiana, Mississippi, Alabama) report among the lowest per-capita losses. As the caveats below note, reported figures depend on awareness and reporting behavior, which this report cannot measure state by state, so lower reported numbers should not be read as lower true risk.

What These Rankings Don’t Capture

Two important caveats apply to all state rankings in this report:

-

These are reported numbers. If reporting rates vary by state, and they almost certainly do, then states with better awareness and easier reporting mechanisms may appear worse than states where victims suffer in silence.

-

These figures cover four crime types. The FBI’s IC3 data used in this analysis covers tech support, investment, romance, and government impersonation scams. Other forms of elder fraud, such as lottery scams, grandparent scams, and extortion, are not included.

Even with these caveats, the data points in one direction: no reporting jurisdiction is untouched, and reported losses rose in every one over the five years.

In Chapter 3, we examine the four major scam categories driving these losses, and reveal how criminal tactics have shifted dramatically over five years.

Data Sources for Chapter 2:

- FBI Internet Crime Complaint Center (IC3), Elder Fraud Reports, 2021–2025

- U.S. Census Bureau, American Community Survey 5-Year Estimates, 2019–2023 (population aged 65+)

- seniors.hcsk.org analysis: per-capita calculations and growth rate analysis

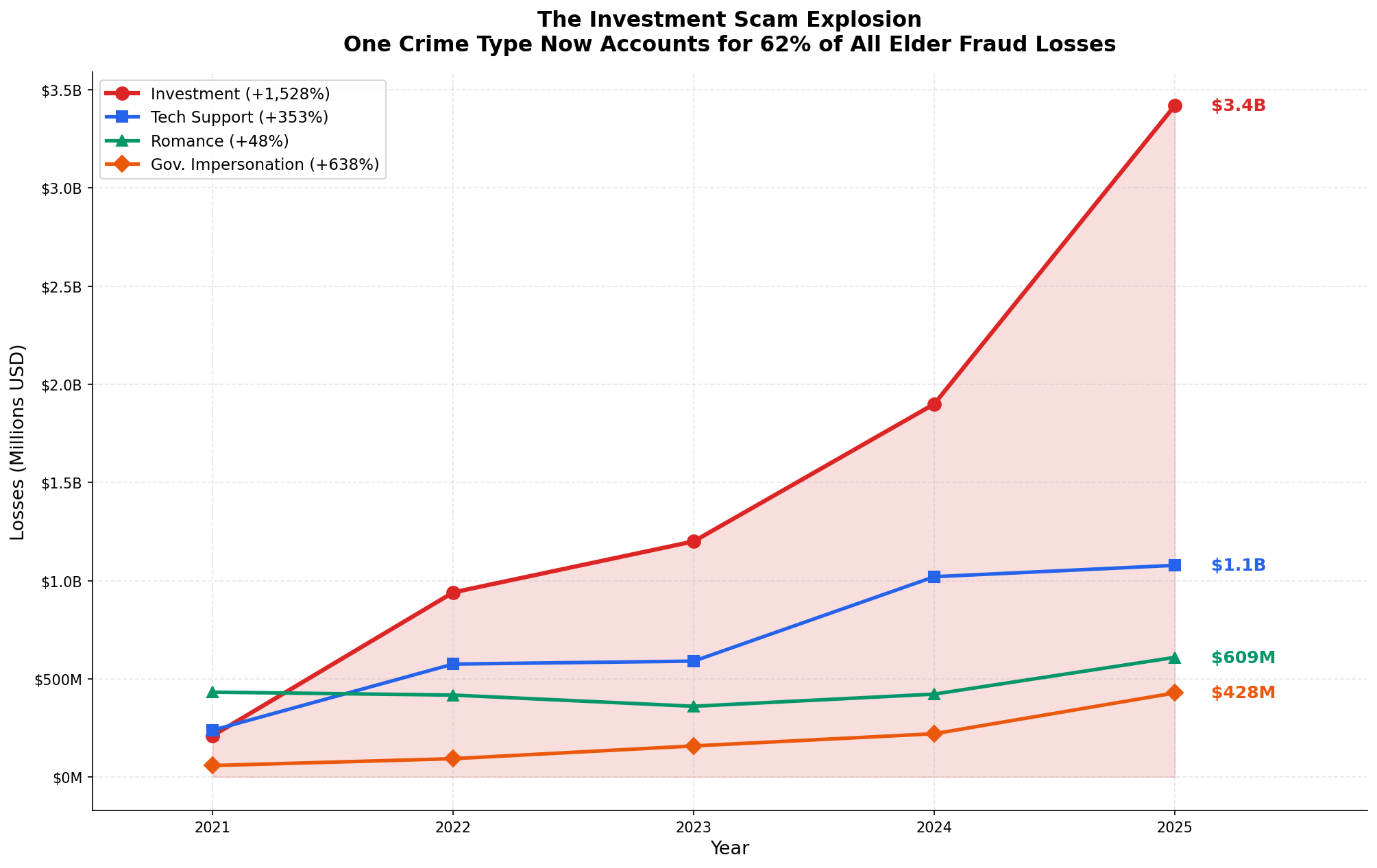

Chapter 3: The Four Scams That Account for Most Elder Fraud Losses

In 2021, investment scams cost seniors aged 60 and over $239 million and $3.519 billion in 2025. That is roughly a fifteen-fold increase in five years.

A Shifting Landscape

Not all scams are created equal, and not all scams age the same way. Over the past five years, the composition of elder fraud in America has undergone a dramatic transformation. One crime type has grown faster than any other, roughly fifteen-fold in five years. Another has quietly declined in volume while growing more sophisticated. Two others have surged in ways that reflect broader shifts in technology and social behavior.

Understanding these four scam categories, how they work, how they’re evolving, and how they differ from one another, is essential for anyone trying to protect older adults or allocate resources to fight fraud.

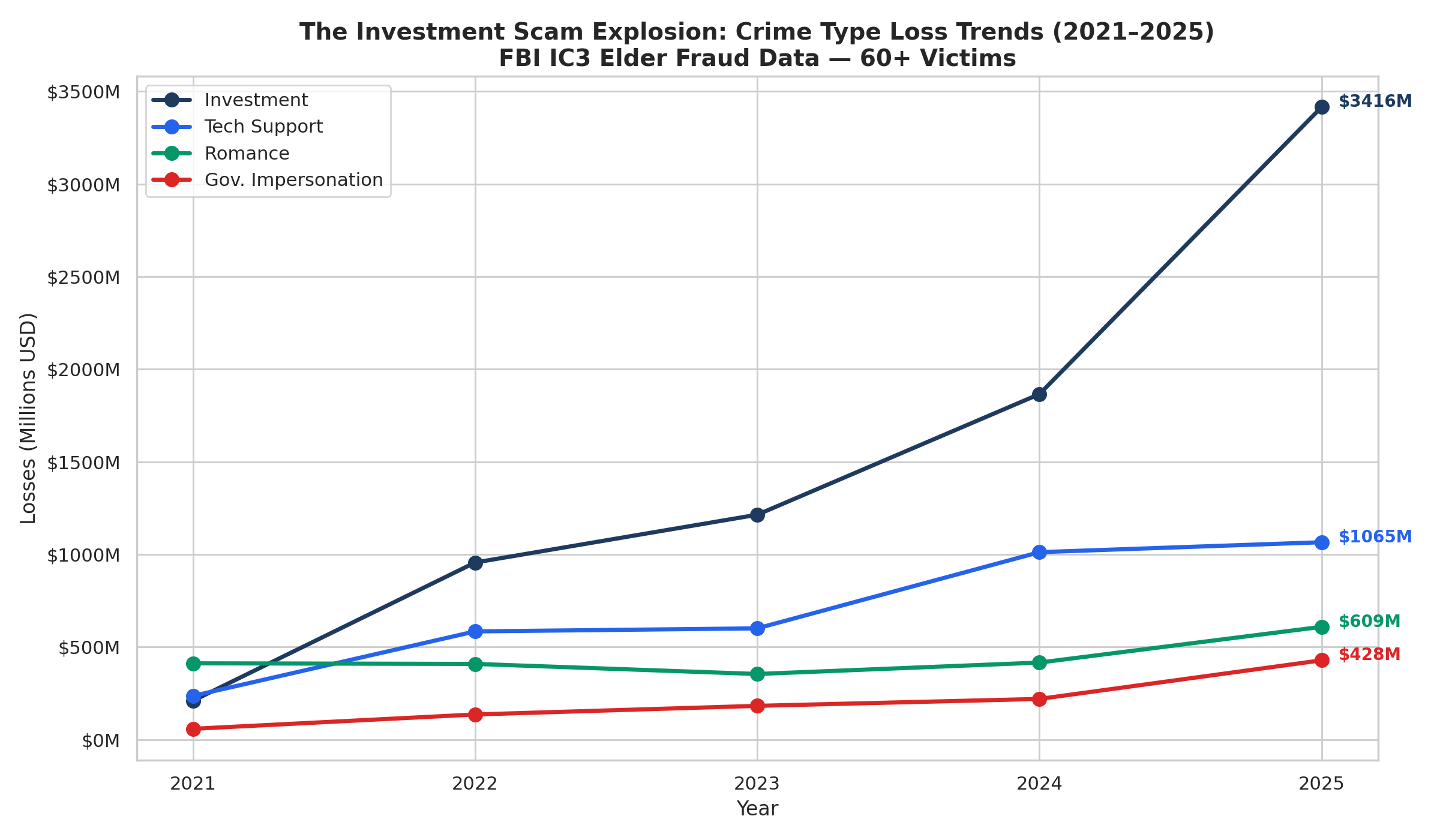

Crime-type loss trends, 2021 to 2025. Source: FBI IC3 Elder Fraud Reports, four major scam categories, victims aged 60+.

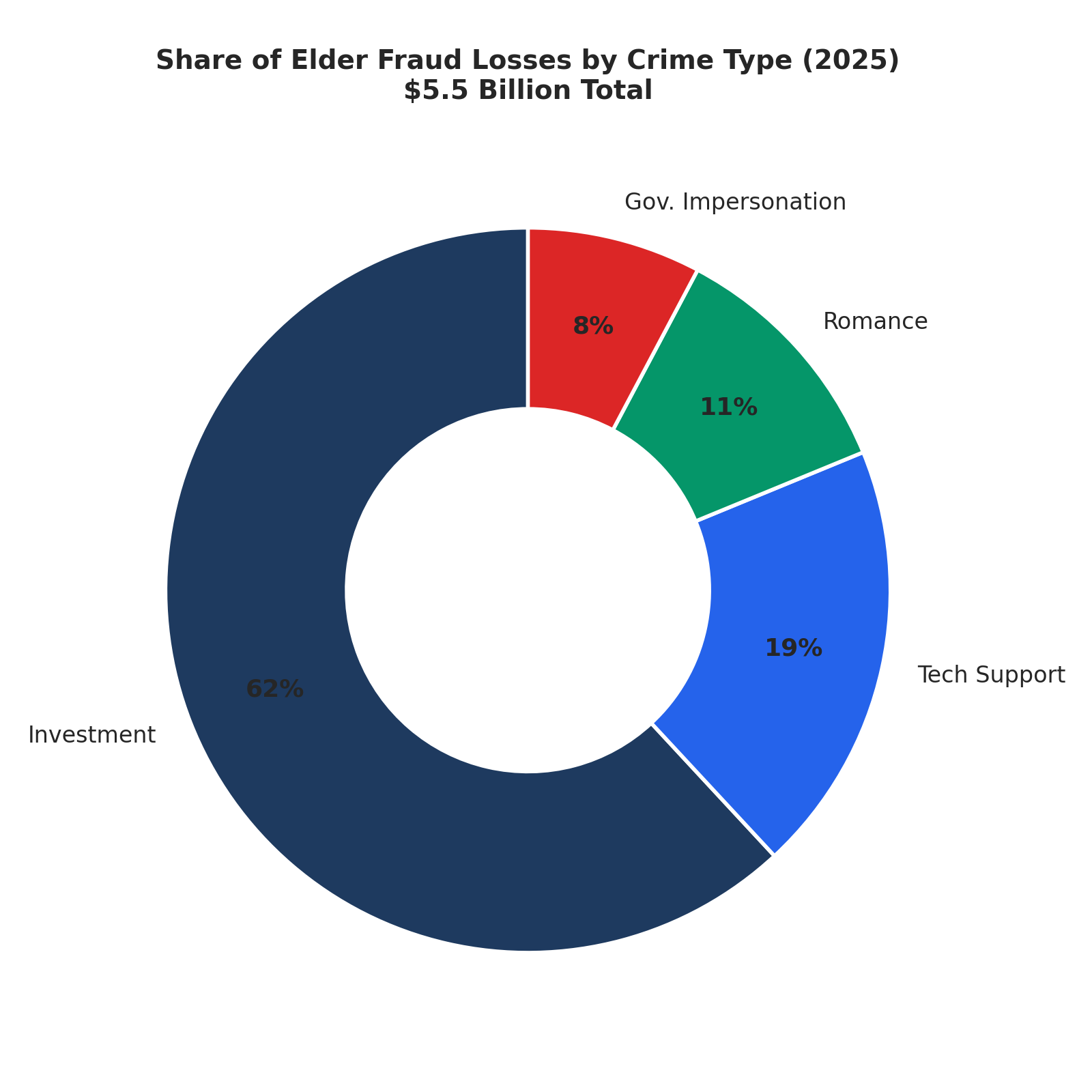

Share of elder fraud losses by crime type, 2025. Source: FBI IC3 Elder Fraud Report 2025, four major scam categories, victims aged 60+.

A note on the two FBI elder-fraud datasets used in this chapter. Section headings for each scam category cite FBI national elder-fraud totals from the IC3 Annual Report’s 60+ chapter (e.g., 2025 investment scams: $3.519 billion / 16,926 complaints). The per-year trend tables that follow use state-aggregated totals built up from the 52 FBI IC3 state files. The two differ slightly: by category and year, the national figure runs a little higher or a little lower than the state-file sum (for example, in 2025 the national investment total runs slightly higher, while in 2024 it runs slightly lower), because the national 60+ chapter and the per-state files aggregate and categorize complaints differently. Both are FBI IC3 figures; we cite each consistently to its own basis rather than mixing them. The trend tables in this chapter carry the state-aggregated category totals; the national 60+ chapter figures are the ones cited in each section heading above.

1. Investment Scams: The Dominant Threat

2025 losses (FBI IC3 Annual Report, 60+ chapter): $3.519 billion | 16,926 complaints | 45% of $7.748B total elder fraud losses

Investment scams are no longer one of four major threats to seniors. They are now the single largest category of elder fraud losses. In 2025, investment fraud accounted for the largest share of elder fraud losses tracked by the FBI, and its five-year growth has been the steepest in the entire elder-fraud category set.

The Numbers Show Steep, Sustained Growth

| Year | Victims | Losses | Avg. Loss Per Victim |

|---|---|---|---|

| 2021 | 1,747 | $210M | $119,863 |

| 2022 | 4,204 | $956M | $227,283 |

| 2023 | 5,925 | $1,214M | $204,904 |

| 2024 | 9,969 | $1,865M | $187,130 |

| 2025 | 16,831 | $3,416M | $203,000 |

Table values are aggregated from FBI IC3 state-level files (the basis for this report’s state-level rankings). For investment scams, the FBI’s annual Elder Fraud Report cites slightly higher national 60+ totals, $239 million in 2021 and $3.519 billion in 2025, reflecting differences in how the national chapter and the per-state files aggregate and categorize complaints (see the dataset note above).

Verified against the FBI IC3 2025 Annual Report 60+ chapter, elder investment losses grew +92 percent year-over-year from 2024 ($1.834 billion) to 2025 ($3.519 billion). Average loss per complaint in 2025 (national 60+ basis) was approximately $208,000, by far the most financially devastating category. A single successful investment scam can destroy a lifetime of savings in weeks.

How It Works

The modern investment scam targeting seniors has evolved far beyond the old boiler-room cold call. Today’s operations typically follow a pattern known as “pig butchering” (sha zhu pan), a term coined by the criminal networks that run them, referring to the practice of “fattening” a victim before “slaughtering” them. The six stages below are a composite drawn from documented cases and FBI and DOJ descriptions of pig butchering; specific amounts and timelines vary.

Stage 1, The Approach. The scammer makes initial contact, most commonly through social media or dating apps. The initial message may appear to be a wrong number, a friend request, or a response to a post in an investment group. There is no mention of money.

Stage 2, The Relationship. Over days or weeks, the scammer builds rapport. Conversations are warm, personal, and frequent. The scammer presents themselves as successful, financially savvy, and genuinely interested in the victim’s well-being. For older adults, these conversations often fill a genuine social void.

Stage 3, The Introduction. The scammer casually mentions their own investment success, often in cryptocurrency. They offer to “teach” the victim or share access to a “private” trading platform. The platform looks professional, complete with real-time charts, account dashboards, and customer service chat.

Stage 4, The Hook. The victim makes a relatively small initial investment, commonly a few hundred to a few thousand dollars. The fake platform shows immediate, impressive returns and the dashboard may display large fabricated gains, encouraging the victim to invest more.

Stage 5, The Escalation. Encouraged by apparent returns, the victim invests larger amounts, often liquidating retirement accounts, taking out home equity loans, or borrowing from family. The platform’s fabricated balance continues to climb.

Stage 6, The Slaughter. When the victim attempts to withdraw funds, they are told they must first pay “taxes”, “verification fees”, or “unlock charges”. These demands escalate until the victim either runs out of money or realizes the fraud. By this point, all invested funds have been transferred overseas through multiple cryptocurrency wallets and are unrecoverable.

Why Seniors Are Disproportionately Targeted

The FTC reports that older adults are actually much less likely than younger adults to report a loss to an investment scam. Yet investment scams generate the highest aggregate losses for older adults of any fraud type. This apparent paradox reveals the reality: when seniors do fall victim, they lose far more money.

The reason is straightforward. Older Americans are more likely to have accumulated substantial savings, retirement accounts, home equity, pension payouts, and are more likely to make large financial decisions without consulting others. The average investment scam loss for a senior exceeds $200,000. For younger adults, it is significantly lower.

The Role of Social Media

The FTC found that social media is now the leading contact method for investment scams among all age groups. For older adults, this represents a fundamental shift. Five years ago, most investment fraud targeting seniors came through phone calls or email. Today, the attack begins with a Facebook message, an Instagram comment, or a WhatsApp group invitation.

2. Tech Support Scams: Declining Volume, Evolving Tactics

2025 losses (FBI IC3 Annual Report, 60+ chapter): $1.041 billion | 21,333 complaints | 13% of $7.748B total elder fraud losses

Tech support scams remain the second-largest financial-loss category by aggregate dollars among the four tracked categories (and the largest of the four by complaint volume). But their trajectory tells a more complex story than the raw numbers suggest.

Trend Analysis

| Year | Victims | Losses | Avg. Loss Per Victim |

|---|---|---|---|

| 2021 | 13,723 | $235M | $17,154 |

| 2022 | 17,693 | $584M | $32,994 |

| 2023 | 18,172 | $600M | $33,034 |

| 2024 | 18,735 | $1,012M | $54,003 |

| 2025 | 23,271 | $1,065M | $45,778 |

Trend table: state-aggregated FBI IC3 totals. The FBI national 60+ figure for 2025 (cited in the section heading above) is $1.041 billion / 21,333 complaints; see the dataset note at the top of this chapter.

While total losses have grown from $235 million to over $1 billion, the rate of growth has slowed significantly compared to investment scams. The victim count has plateaued near 18,000–23,000 per year. What has changed is the average loss per victim, which has nearly tripled, from $17,154 in 2021 to $45,778 in 2025.

This rising per-victim loss is consistent with several non-exclusive drivers: more effective extraction tactics, a shift toward higher-balance targets, or the reclassification of large hybrid “Phantom Hacker” losses into this category (see “A Notable Exception” below). The aggregate data cannot distinguish among them.

The “Phantom Hacker” Evolution

The FBI issued a specific warning in 2023 about a new variant called the “Phantom Hacker” scam, which combines tech support fraud with government impersonation in a devastating three-stage attack:

-

The Tech Support Call. The victim receives a pop-up warning or phone call claiming their computer is compromised. A “technician” gains remote access and shows the victim that their financial accounts are “at risk”.

-

The Bank Impersonation. A second caller, posing as the victim’s bank, confirms that the accounts are under attack and instructs the victim to transfer funds to a “safe” account for protection.

-

The Government Impersonation. A third caller, claiming to be from the FBI, Treasury, or Federal Reserve, validates the previous calls and provides wire transfer instructions to a “government-secured” account.

Each stage builds on the authority established in the previous call. By the time the third caller contacts the victim, they have already spoken with two “officials” who confirmed the threat. The psychological pressure is immense.

The FTC reported that older adults are five times more likely than younger adults to report losing money on a tech support scam, the largest such gap among the fraud types where older adults are more likely to report.

A Notable Exception

Despite the FTC reporting a 9% decrease in aggregate tech support losses for older adults in its Sentinel data for 2024, the FBI’s IC3 data shows continued growth through 2025. This discrepancy reflects differences in how the two systems collect and categorize data. The FBI and FTC collect data through entirely different channels: IC3 accepts complaints filed directly by victims or their representatives, while the FTC’s Sentinel Network aggregates reports from multiple sources including state attorneys general, the BBB, and other agencies. The two systems use different category definitions: what one classifies as “tech support” may overlap with the other’s “business impersonation”. Additionally, hybrid scams like Phantom Hacker, which combine tech support tactics with government impersonation, may be categorized differently depending on which agency receives the report and which stage of the scam the victim describes. Readers should treat both datasets as valid but complementary, each capturing a different slice of the same underlying problem.

3. Romance Scams: Months of Trust, Minutes of Theft

2025 losses (FBI IC3 Annual Report, 60+ chapter, Confidence/Romance): $584 million | 10,188 complaints | 8% of $7.748B total elder fraud losses

Romance scams occupy a unique position in the elder fraud landscape. They are not the largest category by dollar amount, nor the fastest growing. But because they exploit months of cultivated emotional trust, the personal harm reaches well beyond the dollars lost; victims often describe lasting shame and grief alongside the money.

Trend Analysis

| Year | Victims | Losses | Avg. Loss Per Victim |

|---|---|---|---|

| 2021 | 7,212 | $412M | $57,068 |

| 2022 | 6,835 | $408M | $59,730 |

| 2023 | 6,770 | $354M | $52,286 |

| 2024 | 9,447 | $416M | $44,011 |

| 2025 | 11,557 | $609M | $52,672 |

Trend table: state-aggregated FBI IC3 totals. The FBI national 60+ figure for 2025 (cited in the section heading above) is $584 million / 10,188 complaints; see the dataset note at the top of this chapter.

Romance scams dipped in both victims and losses between 2021 and 2023, potentially reflecting increased public awareness. But the numbers surged in 2024 and again in 2025, driven in part by AI tools that make it easier to create convincing fake personas and maintain multiple “relationships” simultaneously (see Chapter 4).

The Long Con

Unlike other scam types that operate on a timeline of hours or days, romance scams unfold over weeks or months. The scammer invests significant time building emotional trust before any mention of money. This makes them uniquely difficult to interrupt.

Typical patterns observed in our news corpus analysis:

- Military impersonation remains common, scammers claim to be deployed soldiers who cannot video-call due to “security restrictions”

- Professional personas, doctors, engineers, or oil rig workers in remote locations explain why they cannot meet in person

- The crisis, after weeks of emotional bonding, the scammer introduces a financial emergency: a medical bill, a frozen bank account, a customs fee for a package

- Graduated requests, initial asks are small ($200–$500), building trust that the money will be “repaid”. Requests escalate over time

- Isolation tactics, the scammer encourages the victim to keep the relationship private, warning that “friends and family won’t understand”

The FTC found that older adults are 39% more likely than younger adults to report romance scam losses, and that romance scams accounted for 28% of all social-media-initiated fraud losses for older adults.

The Scale of the Enterprise

A federal prosecution in the Southern District of New York illustrates the enterprise-level scale of modern romance fraud. A defendant was convicted at jury trial in 2024 and sentenced to 13 years in federal prison after laundering nearly $12 million in stolen funds through ten bank accounts in the Bronx, New York. Between 2020 and 2022, the defendant received money from more than 40 victims, many of them older adults, who were manipulated through fabricated online relationships. The defendant was ordered to forfeit $11.7 million and pay about $7.7 million in restitution. At trial, at least four older victims testified about how they had been deceived.

The Convergence With Investment Scams

An increasingly common variant combines romance and investment fraud. The scammer builds a romantic relationship, then introduces the victim to a “lucrative” investment opportunity. This hybrid approach, sometimes called a “romance-baited investment scam”, appears in the FBI data under either or both categories, potentially undercounting both.

4. Government Impersonation: Exploiting Fear of Authority

2025 losses (FBI IC3 Annual Report, 60+ chapter): $413 million | 8,628 complaints | 5% of $7.748B total elder fraud losses

Government impersonation scams have experienced the second-steepest growth trajectory of any major category over five years, behind only investment. State-aggregated FBI IC3 totals for elder government-impersonation losses grew from $58 million in 2021 to $428 million in 2025, a +638 percent five-year increase. Year-over-year growth from 2024 to 2025 was particularly steep, +99 percent at the FBI national level ($208M → $413M elder gov-imp losses in the IC3 Annual Report’s 60+ chapter), making it the fastest-accelerating major category in the most recent year.

Trend Analysis

| Year | Victims | Losses | Avg. Loss Per Victim |

|---|---|---|---|

| 2021 | 3,187 | $58M | $18,144 |

| 2022 | 3,303 | $135M | $40,951 |

| 2023 | 3,743 | $182M | $48,569 |

| 2024 | 6,939 | $219M | $31,571 |

| 2025 | 11,845 | $428M | $36,130 |

Trend table: state-aggregated FBI IC3 totals. The FBI national 60+ figure for 2025 (cited in the section heading above) is $413 million / 8,628 complaints; see the dataset note at the top of this chapter.

Victim counts have roughly quadrupled since 2021 (from 3,187 to 11,845); losses have grown more than seven-fold over the same period (from $58 million to $428 million, a +638 percent increase). The IC3 annual report shows government impersonation elder losses nearly doubled year-over-year in 2025 ($413M vs. $208M in 2024, a 99% increase), making it the fastest-accelerating major category in the most recent year. The average loss per victim has settled around $36,000, lower than investment scams but still devastating for a retiree on a fixed income.

The Playbook

Government impersonation scams exploit a simple psychological principle: most people, especially older Americans who grew up in an era of greater institutional trust, feel compelled to comply with perceived authority.

The most common variations include:

- IRS scams, threatening arrest for unpaid taxes, demanding immediate payment via gift cards or wire transfer

- Social Security scams, claiming the victim’s SSN has been “suspended” or linked to criminal activity

- Medicare scams, demanding payment for supposed coverage gaps or threatening benefit cancellation

- Law enforcement scams, claiming there is a warrant for the victim’s arrest that can be resolved with a payment

- FTC impersonation, ironically, scammers now impersonate the very agency investigating fraud, telling victims their accounts are “at risk” and must be moved to “protected” accounts

The FTC notes that these scams increasingly blur the line with business impersonation. A single attack may involve callers claiming to represent Microsoft, then the victim’s bank, then the FBI, in sequence. The Phantom Hacker variant described above is a textbook example of this convergence.

The Courier Network

An increasingly common, and increasingly brazen, variant involves physical couriers who arrive at victims’ homes to collect cash or gold. Victims are instructed to withdraw their savings, convert them to gold bars or cash, package them, and hand them to a “government agent” who will appear at their door. The FBI tracked $311.8 million in gold courier scam losses across approximately 725 complaints in 2025 (all ages, per the FBI’s 2025 Internet Crime Report).

DOJ prosecutions have begun to dismantle these networks. In the Western District of Texas, a courier was sentenced to 97 months in federal prison on February 20, 2025 for a role in an operation tied to nearly $7 million in victim losses. A second defendant in the same scheme received 63 months on June 26, 2025; that defendant and a third co-defendant were tied to approximately $3 million in victim losses. A fourth defendant, who coordinated the receipt of victim property from couriers nationwide and from overseas co-conspirators, was indicted in May 2025 and, per the DOJ’s 2025 EAPPA report, has been tied to between approximately $150 million and $200 million in victim losses, among the largest individual loss figures cited in that report.

The Gift Card Connection

Government impersonation scams are the primary driver of gift card payments in elder fraud. Victims are told to purchase gift cards from retailers and read the codes to the caller as “payment” or “verification”. This payment method is virtually impossible to trace or recover.

The FTC found that older adults are 36 percent more likely than younger adults to report government impersonation losses, and that government impersonation was the #3 fraud type by total dollars lost among older adults in FTC Sentinel data.

The SSA Imposter Quarterly Picture

The Social Security Administration’s Office of Inspector General has published quarterly scam reports continuously since July 2021. Across 17 quarters of data (Issues 2–18, covering Q4 FY 2021 through Q4 FY 2025), the SSA OIG documents the dominant variant within government impersonation: someone calling, emailing, or texting claiming to be from the Social Security Administration. The quarterly data reveals two important counter-trends to the broader elder-fraud growth story:

- SSA-related scam allegations have declined dramatically from their FY 2019–FY 2021 peak. During the peak quarters, SSA OIG was receiving more than 150,000 scam allegations per quarter, in some quarters over 225,000. From April 2022 onward, the agency has received fewer than 10,000 SSA-related scam allegations per month (roughly 30,000 or fewer per quarter), an approximately 80–90 percent decline from peak.

- Despite the decline, SSA-impersonation remains a top reported government-imposter scam type to the FTC. The decline reflects partial success of public-awareness campaigns and law-enforcement disruption, not the elimination of the threat.

The pattern is a useful counter-example to the broader narrative that all elder-fraud categories are growing without limit. Targeted federal-state-private campaigns can bend the curve on a specific scam type. The lesson is not that the SSA imposter scam is solved, it is that dedicated, coordinated federal-state-private response on a single threat can produce measurable reduction. Source: SSA OIG, Quarterly Scam Reports Issues 2–18 (2021–2025).

The Medicare-Adjacent Hospice Fraud Variant

A second variant within the government-impersonation category that warrants attention is the Medicare-hospice enrollment scam, in which fraudsters enroll Medicare beneficiaries into hospice care without the beneficiary’s knowledge or consent, sometimes through door-to-door “Medicare benefit review” approaches. The victim may not realize they have been enrolled in hospice (which under Medicare rules cancels coverage for curative treatments) until they next attempt to access regular medical care. (HHS OIG has long warned about hospice fraud in a different form: its 1998 Special Fraud Alert on nursing-home arrangements with hospices documents illegal kickbacks paid to influence hospice enrollment, a provider-side scheme distinct from the consumer-facing enrollment fraud described here.)

The HHS OIG hotline for reporting Medicare fraud is 1-800-HHS-TIPS (1-800-447-8477). The Senior Medicare Patrol national locator (1-877-808-2468) connects beneficiaries to their state SMP for one-on-one help. See Chapter 6 for the broader inventory of federal actors involved in Medicare fraud response.

The Veteran-Targeted Variant

Veterans, service members, and their survivors face a government-impersonation subtype built around earned benefits. Fraudsters impersonating the VA tell veterans they owe money for a benefits “overpayment”, use stolen personal information to redirect benefit payments to accounts they control, or operate as “claims predators” who unlawfully charge fees to “help” file an initial VA claim, assistance that VA-accredited representatives and Veterans Service Organizations provide for free. Because the lure is the veteran’s own benefits and the impersonated authority is one they have every reason to trust, these schemes are both convincing and especially corrosive. Related schemes target the same population, including “pension poaching” (advisers who promise to boost benefits by restructuring assets into high-fee annuities or trusts) and “benefits buyout” offers that trade a lump sum for the far greater lifetime value of a veteran’s payments. In a May 22, 2026 advisory, the Arizona Attorney General catalogued ten such schemes targeting the state’s veterans. The VA’s dedicated fraud line, VSAFE (vsafe.gov; 1-833-38V-SAFE / 1-833-388-7233), is the correct reporting channel. See Chapter 9 for how a single national front door builds on the VSAFE model.

Crime Type Migration: What Five Years of Data Reveal

Viewed together, the five-year trends reveal a criminal ecosystem that is constantly adapting.

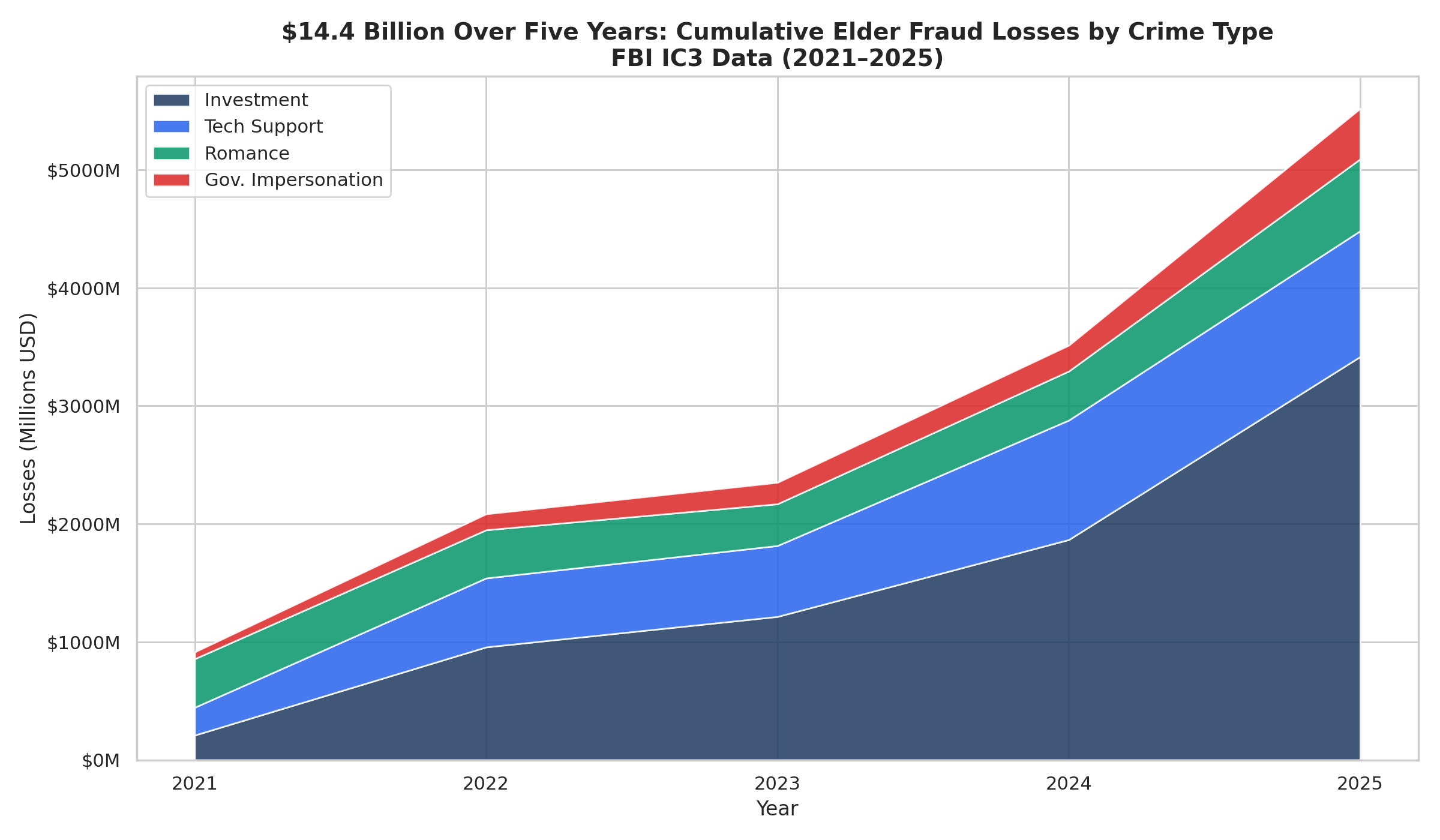

Five-year stacked losses by crime type, 2021 to 2025. Source: FBI IC3 Elder Fraud Reports, four major scam categories.

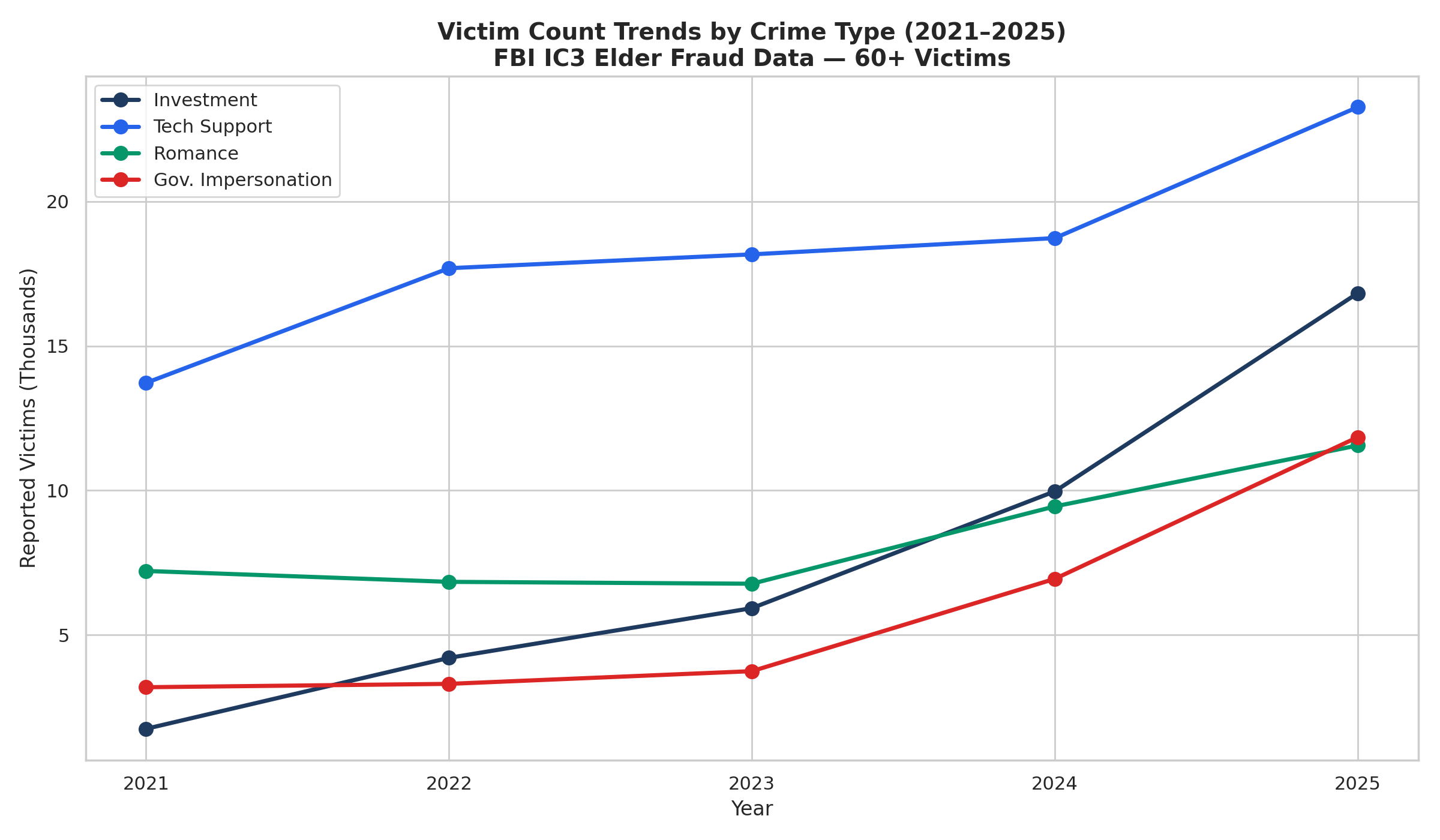

Crime-type victim trends, 2021 to 2025. Source: FBI IC3 Elder Fraud Reports, four major scam categories, victims aged 60+.

The FTC’s Complementary Data

The FTC’s Sentinel data provides a complementary view of the same landscape, with different categorization. For adults 60 and over in 2024, FTC data shows: investment scams $744 million (+38% YoY), business impersonation $377 million (+21%), government impersonation $375 million (+47%), romance scams $329 million (+19%), and tech support $159 million (-9%). The 47% jump in FTC-reported government-impersonation losses (2023 to 2024) echoes the steep IC3 trend for this category (IC3 elder gov-imp losses rose roughly 99 percent nationally from 2024 to 2025), reinforcing that government impersonation is among the fastest-accelerating fraud types.

Key Shifts

Investment scam loss growth, 2021 to 2025. Source: FBI IC3 Elder Fraud Reports, investment-scam category, victims aged 60+.

The investment scam explosion is the defining story of this five-year period. In 2021, investment scams accounted for $239 million; by 2025 they were by far the largest category at $3.519 billion, or 45% of all elder fraud losses (and, on the state-aggregated basis used in this report’s trend tables, about 62% of the four tracked categories). This roughly fifteen-fold increase is the largest such jump on record across the four scam categories tracked by FBI IC3.

Tech support scams have plateaued in volume but increased in per-victim severity. The number of victims has grown modestly, but the average loss per victim has nearly tripled. This rising per-victim loss, alongside only modest growth in victim count, means the category’s growth is now driven mainly by larger losses per case rather than by more victims.

Romance scams recovered from a mid-period dip. After declining in 2022–2023, they surged in 2024–2025. A likely catalyst is the spread of AI tools: widely available chatbots and deepfake generators have dramatically reduced the effort required to maintain convincing romantic personas at scale (see Chapter 4).

Government impersonation is the fastest-accelerating category in the most recent year, though it started from the smallest base. Its +638 percent five-year growth, second only to investment, combined with its integration into multi-stage scams like Phantom Hacker, makes it the category most likely to continue accelerating.

The Convergence Trend

Perhaps the most important insight from five years of data is that these categories are converging. The Phantom Hacker combines tech support with government impersonation. Romance-baited investment scams combine romance with investment fraud. Business impersonation scams (tracked separately by the FTC) share tactics with both tech support and government impersonation.

The scam of 2026 is not neatly categorizable. It is a multi-stage, multi-persona operation that may involve elements of all four categories in a single attack. This convergence poses a significant challenge for data collection, as crimes that span multiple categories may be undercounted in every category.

Across every category and every hybrid, the point of attack is the same. These scams rarely succeed by breaking into a device; they succeed by breaking into a person’s trust and judgment. The vulnerability is human, not technical; no firewall stops a victim who has been persuaded to send the money themselves. It is why the response in Chapter 9 centers on a message about how people decide, not how they secure a machine.

Beyond the Four: Emerging Categories

While this report tracks four primary crime types, several additional categories deserve attention for their rapid growth:

- Account Takeover (ATO): Approximately 4,700 complaints (all ages, per the FBI’s 2025 Internet Crime Report) totaling $359.7 million in 2025, scammers gain control of victims’ financial accounts and drain them, often through SIM swaps (tricking a phone carrier into moving the victim’s number to a phone the criminal controls, which intercepts security codes) or credential theft.